{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

858 S.D. County educators collect pensions of $100,000+

How much do you like your teachers?

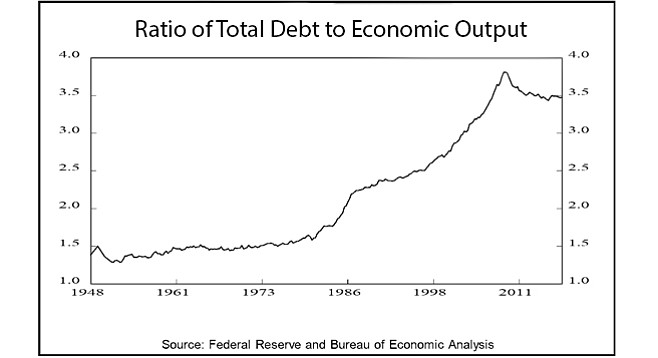

Ratio of debt to output has come down but still high.

Ten years ago, the world narrowly averted a financial disaster. It began with an explosion of low-quality mortgages bundled into putrid-quality financial paper that was awarded the highest-quality rating (AAA). Financial institutions began to collapse. The stock market plunged and the Great Recession ensued. The United States government fleeced the little folks by bailing out the big banks with taxpayer money. Then we wee folk got screwed again when the Federal Reserve dropped interest rates to near zero, meaning that savers got almost no interest. That’s not much better now.

Slowly, the world was saved, mainly by the flood of money and credit. That’s the good news. The bad news is that the federal government is acting as if we are still in recession and need a huge boost. As Ross Starr, professor emeritus and research professor at the University of California at San Diego, points out, the conventional cure for recession is a big federal deficit. But right now, we are at or near full employment. The economy is humming. Even though recessions generally come around every ten years, there is not one on the horizon.

Nonetheless, the Congress has passed a budget that will bring the annual deficit to a startling $1 trillion a year, and that deficit will continue to zoom throughout the 2020s. The Federal Reserve is raising interest rates, and bond buyers are demanding higher rates. The International Monetary Fund recently projected that the United States is the only advanced economy in the world that will see its debt burden worsen in the next five years.

New Jersey–based economist A. Gary Shilling looks at both public and private sector debt and says that total debt in the U.S. is now 3.5 times our total economic output. It takes $3.50 of debt for every dollar of economic output. That’s up from $1.50 in the 1960s and 1970s.

Some economists hope that foreigners will step up their plunking of savings into the American dollar, buying American debt, providing the money that otherwise would be sucked up by the deficit. That’s too big a gamble for Starr to count on. He takes the conventional view: “It is my personal view that with current federal policy we are in for a period of rising inflation and interest rates,” he says. “If inflation takes off [in this cycle], we will see a decline in stock and bond values. This will have a negative effect on the economy.”

Lynn Reaser, chief economist at Point Loma Nazarene University, says it boils down to this: “Our country does not save enough. Individuals and governments cannot continue to live beyond their means. Foreigners save too much and buy our debt.” But will they continue to do so? “If foreigners decide we are not the best place to invest, we have to entice them with higher interest rates or a drop in the value of the dollar, or a combination of the two. These [would be] negatives for the economy. Ultimately, the core of the problem lies with entitlement spending [Social Security, Medicare, Medicaid, etc.]”

State and local debt “is dominated by pension liabilities,” she says. “If investment returns begin to diminish, government services may have to be cut to pay those obligations, or taxes will have to be raised substantially.”

Mike Stolper, retired San Diego financial advisor, says, “A substantial part of debt will be repudiated,” and the first to be dealt with will be state and local debt for public employees. There is a crisis there. Last year, fully 858 retired San Diego County educators collected pensions of $100,000 or more — up 90 percent from 2012, according to TransparentCalifornia.com.

Knowing California as he does, Stolper thinks judges will be kind to educators; that means bondholders will carry the burden of straightening out the pension messes.

At the federal level, he thinks bond buyers (formerly known as bond vigilantes) will be the referees: they will refuse to buy certain bonds unless interest rates are high enough. Then governments will be forced to act. “This will stop the expansion of debt,” says Stolper. Ever since the Federal Reserve sharply lowered rates beginning in 2009, mortgages have been going for 4 percent, sometimes less. “I don’t have to tell you what happens when mortgage rates go to normal — say, to 6 percent. Overall, real estate is most vulnerable.” He thinks President Trump is bringing “a shift to a more [accommodative] business climate. That is what the market likes.” Stocks will be up and down, but he thinks in the long run they will do fine.

But Jim Welsh of San Marcos, who is a macrostrategist and portfolio consultant for Seattle’s Smart Portfolios, disagrees with Stolper. “Sooner or later, the piper has to be paid,” says Welsh. “As debt continues to rise, we get less and less economic bang for the buck, as the ratio of $3.50 of debt for $1 of output shows. A very, very difficult time is coming.” Recessions normally come every ten years and one is due, but the federal government in making forecasts doesn’t even take one into account.

“Since 1980, [corporations’] focus has been on increasing shareholder value. This has come at the expense of wages being paid to workers,” he says. “This is laying the seeds for a weak economy and potentially unrest.” One result is the spread of populism and protectionism. Middle-class incomes have been stymied for several decades. Within a few years, Welsh can see a steep recession and stock market “that could lose 50 to 80 percent of its value.”

But Gary Shilling, a major student in the relationship between debt and the economy, and also generally more pessimistic than most of his peers, is no longer fretting about too much debt. He writes, “The chances of another 2008 financial crisis are probably remote. If history is any guide, the next financial trauma will appear elsewhere, just as the savings-and-loan crisis of the late 1980s was not repeated but followed by the dot-com stock bubble collapse of the early 2000s. Then came the rise and fall of [low quality] mortgages.”

Shilling doubts that high interest rates and inflation are on the horizon. The Federal Reserve wants 2 percent inflation, but it stubbornly stays lower. Labor markets are not tight. Economists are looking only at the unemployment rate, which is statistically misleading. In 1981, when long-term interest rates were above 15 percent, he predicted, “We’re entering the bond rally of a lifetime.” He was right.

What’s next? Who knows?■

Here's something you might be interested in.

858 S.D. County educators collect pensions of $100,000+

How much do you like your teachers?

858 S.D. County educators collect pensions of $100,000+

How much do you like your teachers?

Ratio of debt to output has come down but still high.

Ten years ago, the world narrowly averted a financial disaster. It began with an explosion of low-quality mortgages bundled into putrid-quality financial paper that was awarded the highest-quality rating (AAA). Financial institutions began to collapse. The stock market plunged and the Great Recession ensued. The United States government fleeced the little folks by bailing out the big banks with taxpayer money. Then we wee folk got screwed again when the Federal Reserve dropped interest rates to near zero, meaning that savers got almost no interest. That’s not much better now.

Slowly, the world was saved, mainly by the flood of money and credit. That’s the good news. The bad news is that the federal government is acting as if we are still in recession and need a huge boost. As Ross Starr, professor emeritus and research professor at the University of California at San Diego, points out, the conventional cure for recession is a big federal deficit. But right now, we are at or near full employment. The economy is humming. Even though recessions generally come around every ten years, there is not one on the horizon.

Nonetheless, the Congress has passed a budget that will bring the annual deficit to a startling $1 trillion a year, and that deficit will continue to zoom throughout the 2020s. The Federal Reserve is raising interest rates, and bond buyers are demanding higher rates. The International Monetary Fund recently projected that the United States is the only advanced economy in the world that will see its debt burden worsen in the next five years.

New Jersey–based economist A. Gary Shilling looks at both public and private sector debt and says that total debt in the U.S. is now 3.5 times our total economic output. It takes $3.50 of debt for every dollar of economic output. That’s up from $1.50 in the 1960s and 1970s.

Some economists hope that foreigners will step up their plunking of savings into the American dollar, buying American debt, providing the money that otherwise would be sucked up by the deficit. That’s too big a gamble for Starr to count on. He takes the conventional view: “It is my personal view that with current federal policy we are in for a period of rising inflation and interest rates,” he says. “If inflation takes off [in this cycle], we will see a decline in stock and bond values. This will have a negative effect on the economy.”

Lynn Reaser, chief economist at Point Loma Nazarene University, says it boils down to this: “Our country does not save enough. Individuals and governments cannot continue to live beyond their means. Foreigners save too much and buy our debt.” But will they continue to do so? “If foreigners decide we are not the best place to invest, we have to entice them with higher interest rates or a drop in the value of the dollar, or a combination of the two. These [would be] negatives for the economy. Ultimately, the core of the problem lies with entitlement spending [Social Security, Medicare, Medicaid, etc.]”

State and local debt “is dominated by pension liabilities,” she says. “If investment returns begin to diminish, government services may have to be cut to pay those obligations, or taxes will have to be raised substantially.”

Mike Stolper, retired San Diego financial advisor, says, “A substantial part of debt will be repudiated,” and the first to be dealt with will be state and local debt for public employees. There is a crisis there. Last year, fully 858 retired San Diego County educators collected pensions of $100,000 or more — up 90 percent from 2012, according to TransparentCalifornia.com.

Knowing California as he does, Stolper thinks judges will be kind to educators; that means bondholders will carry the burden of straightening out the pension messes.

At the federal level, he thinks bond buyers (formerly known as bond vigilantes) will be the referees: they will refuse to buy certain bonds unless interest rates are high enough. Then governments will be forced to act. “This will stop the expansion of debt,” says Stolper. Ever since the Federal Reserve sharply lowered rates beginning in 2009, mortgages have been going for 4 percent, sometimes less. “I don’t have to tell you what happens when mortgage rates go to normal — say, to 6 percent. Overall, real estate is most vulnerable.” He thinks President Trump is bringing “a shift to a more [accommodative] business climate. That is what the market likes.” Stocks will be up and down, but he thinks in the long run they will do fine.

But Jim Welsh of San Marcos, who is a macrostrategist and portfolio consultant for Seattle’s Smart Portfolios, disagrees with Stolper. “Sooner or later, the piper has to be paid,” says Welsh. “As debt continues to rise, we get less and less economic bang for the buck, as the ratio of $3.50 of debt for $1 of output shows. A very, very difficult time is coming.” Recessions normally come every ten years and one is due, but the federal government in making forecasts doesn’t even take one into account.

“Since 1980, [corporations’] focus has been on increasing shareholder value. This has come at the expense of wages being paid to workers,” he says. “This is laying the seeds for a weak economy and potentially unrest.” One result is the spread of populism and protectionism. Middle-class incomes have been stymied for several decades. Within a few years, Welsh can see a steep recession and stock market “that could lose 50 to 80 percent of its value.”

But Gary Shilling, a major student in the relationship between debt and the economy, and also generally more pessimistic than most of his peers, is no longer fretting about too much debt. He writes, “The chances of another 2008 financial crisis are probably remote. If history is any guide, the next financial trauma will appear elsewhere, just as the savings-and-loan crisis of the late 1980s was not repeated but followed by the dot-com stock bubble collapse of the early 2000s. Then came the rise and fall of [low quality] mortgages.”

Shilling doubts that high interest rates and inflation are on the horizon. The Federal Reserve wants 2 percent inflation, but it stubbornly stays lower. Labor markets are not tight. Economists are looking only at the unemployment rate, which is statistically misleading. In 1981, when long-term interest rates were above 15 percent, he predicted, “We’re entering the bond rally of a lifetime.” He was right.

What’s next? Who knows?■

Comments