{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Fed shovels money to Wall Street, not Main Street

Central bank creates money for those who already have it.

Is our central bank, the Federal Reserve, trying to help Main Street or Wall Street? On November 11, Andrew Huszar, a former Fed official, charged in the Wall Street Journal that it’s the latter. “I’m sorry, America,” he wrote in an essay dripping with repentance.

He had taken the job of quarterbacking the Fed’s massive bond-purchasing program, called quantitative easing, best known as QE. He was assured it would be “a tool for helping Main Street,” he wrote. But, belatedly, he realized it has been “the greatest backdoor Wall Street bailout of all time.”

While driving short-term interest rates that banks pay down to about zero, the Fed over five years bought $4 trillion of bonds, bringing long-term rates down dramatically, too. Interest rates got so low that bonds and cash became dead money: stocks were the only place to go, and Fed chairman Ben Bernanke admitted that this was one of his motivations. He wanted to drive money out of sleepy instruments and into gamier stocks.

Kelly Cunningham.

Stocks have far more than doubled from their lows of early 2009 and are now at record highs. But following the worst downturn since the 1930s Depression, the economy has suffered one of history’s weakest recoveries. Huszar quotes one well-respected economist who says that the $4 trillion spent on quantitative easing has netted a meager 0.25 percent rise in economic output.

Two days after Huszar’s blockbuster column, Janet Yellen, who is almost certain to be named the next head of the Fed, said she favors continuation of quantitative easing. Stocks rejoiced.

But San Diego economists have mixed views. “It’s refreshing to hear someone being honest about it. QE has not helped the country or Main Street,” says Kelly Cunningham, economist for the National University System Institute for Policy Research. In San Diego, the lower interest rates have boosted housing prices (as if they needed boosting). In the first half of this year, the median price of a San Diego home was $400,000 and median family income $72,300. “The housing price is 5.5 times what income is. That doesn’t pencil out.”

Marney Cox.

At the peak of the bubble in late 2005, San Diego homes sold for 8 times household incomes. Normal is about 4 in coastal California and 2.5 to 3 in the rest of the country. Cunningham suspects that the local housing price boom has come largely from institutional buyers, often purchasing with cash. The wee folks still have trouble getting a mortgage. “QE created dollars for investors,” not average people, says Cunningham.

Marney Cox, chief economist for San Diego Association of Governments (SANDAG), says that quantitative easing “did stabilize the financial community from its free fall” back in the depths of the recession. Without quantitative easing, “the recession would have been longer and deeper, but it is hard to argue that QE is now stimulating the economy. Take a look at the labor force; you can see the economy is weak.” Corporate profits are high because of the low interest rates and companies’ hesitancy to hire. Those factors also boost stocks while Main Street suffers.

Cox notes that at some point, the Fed will have to start selling that $4 trillion in bonds on its balance sheet. Indeed, the stock market falls every time a Fed official even hints that the central bank will have to slow down its monthly bond purchases. Cleaning up that balance sheet “will create additional havoc in the financial community.”

Todd Buchholz.

Cox agrees with Cunningham that investors — not average people — are driving up San Diego housing prices. “The price increase will probably be short-lived,” he says.

Huszar’s essay is “a narrow-minded conspiracy theory,” says Ross Starr, professor of economics at the University of California San Diego. He cites the positives: “Bringing interest rates down or keeping them from going up encourages refinancing of existing mortgages and encourages new construction,” he says. And he notes that in the deepest periods of the recession, the Fed was helping the Treasury finance the economy. Because of the recession, the deficit soared and the Treasury had to sell bonds. By keeping interest rates down, the Fed helped stem a flood of Treasury bonds pouring onto the market and driving interest rates up.

But Starr, too, is not convinced how effective the Fed’s program is now. “There should be a doctoral dissertation on the effectiveness of QE3 [the current bond-buying program] once it is completed,” he says.

Former White House director of economic policy Todd Buchholz says, “It is an irresponsible canard to say that Bernanke and the Fed plotted to put money in the hands of Wall Street fat cats and deny money to Main Street.” Quantitative easing succeeded in “shoving money out the door. If you look at the economy today, there are very few healthy sectors. One has been autos and the other housing — both interest-rate sensitive” and beneficiaries of the QE programs. “If neither housing nor autos had come back, we would be in the midst of a great recession. The economy is still pretty feeble.”

Ross Starr.

Buchholz, founder of a company with an innovative way to teach mathematics to youngsters, notes that Bernanke’s critics said inflation would roar upward and the dollar plummet scarily — but neither happened. However, he believes that quantitative easing “has overstayed its welcome.” The monthly purchases should be reduced. And, he concedes, “There have been victims of QE — older people on fixed incomes and savers have been punished.”

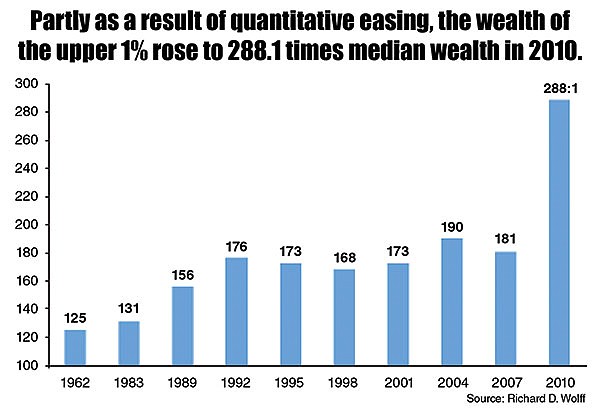

There is one economically destructive aspect to quantitative easing that Huszar didn’t mention. The big run-up in the stock market, combined with the measly interest rates that lower-income people get on their savings, has exacerbated one of our worst economic problems: the wide wealth and income gap between the top 1 percent and the rest of Americans. From 2009 to 2012, incomes of the top 1 percent grew more than 31 percent while incomes of the other 99 percent grew less than half of 1 percent. The top 1 percent now have almost 40 percent of the nation’s financial wealth. Driving up the stock market helps the upper 10 percent, who own 90 percent of stocks, including 401(k) retirement accounts.

And, paradoxically, it is political liberals, the biggest complainers about income inequality, who are leading the cheers for quantitative easing.

Here's something you might be interested in.

Fed shovels money to Wall Street, not Main Street

Central bank creates money for those who already have it.

Fed shovels money to Wall Street, not Main Street

Central bank creates money for those who already have it.

Is our central bank, the Federal Reserve, trying to help Main Street or Wall Street? On November 11, Andrew Huszar, a former Fed official, charged in the Wall Street Journal that it’s the latter. “I’m sorry, America,” he wrote in an essay dripping with repentance.

He had taken the job of quarterbacking the Fed’s massive bond-purchasing program, called quantitative easing, best known as QE. He was assured it would be “a tool for helping Main Street,” he wrote. But, belatedly, he realized it has been “the greatest backdoor Wall Street bailout of all time.”

While driving short-term interest rates that banks pay down to about zero, the Fed over five years bought $4 trillion of bonds, bringing long-term rates down dramatically, too. Interest rates got so low that bonds and cash became dead money: stocks were the only place to go, and Fed chairman Ben Bernanke admitted that this was one of his motivations. He wanted to drive money out of sleepy instruments and into gamier stocks.

Kelly Cunningham.

Stocks have far more than doubled from their lows of early 2009 and are now at record highs. But following the worst downturn since the 1930s Depression, the economy has suffered one of history’s weakest recoveries. Huszar quotes one well-respected economist who says that the $4 trillion spent on quantitative easing has netted a meager 0.25 percent rise in economic output.

Two days after Huszar’s blockbuster column, Janet Yellen, who is almost certain to be named the next head of the Fed, said she favors continuation of quantitative easing. Stocks rejoiced.

But San Diego economists have mixed views. “It’s refreshing to hear someone being honest about it. QE has not helped the country or Main Street,” says Kelly Cunningham, economist for the National University System Institute for Policy Research. In San Diego, the lower interest rates have boosted housing prices (as if they needed boosting). In the first half of this year, the median price of a San Diego home was $400,000 and median family income $72,300. “The housing price is 5.5 times what income is. That doesn’t pencil out.”

Marney Cox.

At the peak of the bubble in late 2005, San Diego homes sold for 8 times household incomes. Normal is about 4 in coastal California and 2.5 to 3 in the rest of the country. Cunningham suspects that the local housing price boom has come largely from institutional buyers, often purchasing with cash. The wee folks still have trouble getting a mortgage. “QE created dollars for investors,” not average people, says Cunningham.

Marney Cox, chief economist for San Diego Association of Governments (SANDAG), says that quantitative easing “did stabilize the financial community from its free fall” back in the depths of the recession. Without quantitative easing, “the recession would have been longer and deeper, but it is hard to argue that QE is now stimulating the economy. Take a look at the labor force; you can see the economy is weak.” Corporate profits are high because of the low interest rates and companies’ hesitancy to hire. Those factors also boost stocks while Main Street suffers.

Cox notes that at some point, the Fed will have to start selling that $4 trillion in bonds on its balance sheet. Indeed, the stock market falls every time a Fed official even hints that the central bank will have to slow down its monthly bond purchases. Cleaning up that balance sheet “will create additional havoc in the financial community.”

Todd Buchholz.

Cox agrees with Cunningham that investors — not average people — are driving up San Diego housing prices. “The price increase will probably be short-lived,” he says.

Huszar’s essay is “a narrow-minded conspiracy theory,” says Ross Starr, professor of economics at the University of California San Diego. He cites the positives: “Bringing interest rates down or keeping them from going up encourages refinancing of existing mortgages and encourages new construction,” he says. And he notes that in the deepest periods of the recession, the Fed was helping the Treasury finance the economy. Because of the recession, the deficit soared and the Treasury had to sell bonds. By keeping interest rates down, the Fed helped stem a flood of Treasury bonds pouring onto the market and driving interest rates up.

But Starr, too, is not convinced how effective the Fed’s program is now. “There should be a doctoral dissertation on the effectiveness of QE3 [the current bond-buying program] once it is completed,” he says.

Former White House director of economic policy Todd Buchholz says, “It is an irresponsible canard to say that Bernanke and the Fed plotted to put money in the hands of Wall Street fat cats and deny money to Main Street.” Quantitative easing succeeded in “shoving money out the door. If you look at the economy today, there are very few healthy sectors. One has been autos and the other housing — both interest-rate sensitive” and beneficiaries of the QE programs. “If neither housing nor autos had come back, we would be in the midst of a great recession. The economy is still pretty feeble.”

Ross Starr.

Buchholz, founder of a company with an innovative way to teach mathematics to youngsters, notes that Bernanke’s critics said inflation would roar upward and the dollar plummet scarily — but neither happened. However, he believes that quantitative easing “has overstayed its welcome.” The monthly purchases should be reduced. And, he concedes, “There have been victims of QE — older people on fixed incomes and savers have been punished.”

There is one economically destructive aspect to quantitative easing that Huszar didn’t mention. The big run-up in the stock market, combined with the measly interest rates that lower-income people get on their savings, has exacerbated one of our worst economic problems: the wide wealth and income gap between the top 1 percent and the rest of Americans. From 2009 to 2012, incomes of the top 1 percent grew more than 31 percent while incomes of the other 99 percent grew less than half of 1 percent. The top 1 percent now have almost 40 percent of the nation’s financial wealth. Driving up the stock market helps the upper 10 percent, who own 90 percent of stocks, including 401(k) retirement accounts.

And, paradoxically, it is political liberals, the biggest complainers about income inequality, who are leading the cheers for quantitative easing.

Comments