{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Brick & mortar vs. Amazon

Mall stores getting Amazonned into deep doo-doo

Regal Cinemas — Amazon-proof?

Fifty years ago, shopping malls were the local gathering places. Days and nights, they were jam-packed with people of all demographic groups. But by 2014, almost 20 percent of American malls were considered in trouble — that is, they had vacancy rates of 10 percent or more. It has gotten worse. Deadmalls.com, the website devoted to the topic, says that a dead mall is one having an “occupancy rate in slow or steady decline of 70 percent or less.” And the website lists them by the dozens, although none is in San Diego County.

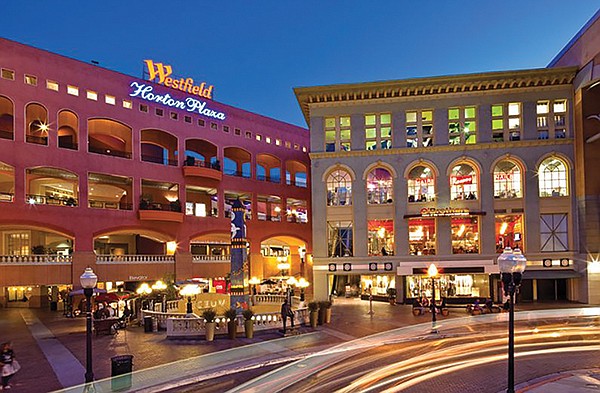

Horton Plaza. Important retailers started deserting it not long after it opened. A huge part of it has been ripped down.

On May 31, the big bank Credit Suisse predicted that 25 percent of malls would be gone in the next five years. Earlier forecasts had also been dire, and results prove them to have been accurate. Malls used to be anchored by big department stores — Sears, JCPenney, Macy’s, and the like.

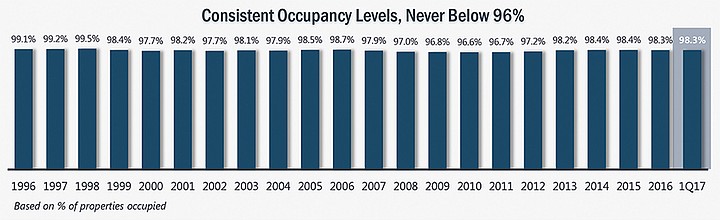

San Diego's Realty Investment Corp. success chart. It is not into malls. It buys freestanding, single-tenant properties. (Click to enlarge)

All are now in deep doo-doo and closing stores, upsetting the malls that relied upon them as consumer draws and sources of revenue. The smaller mall stores, which pay higher rent per square foot than the anchors, are having trouble, further biting into mall revenue and traffic.

Much of this is tied to the American economy. For several decades, income growth has gone mainly to the rich and superrich, while the middle class has shrunk. Malls that appeal to the middle and lower-middle classes are hurting. San Diego has a good example of that economically ruinous trend.

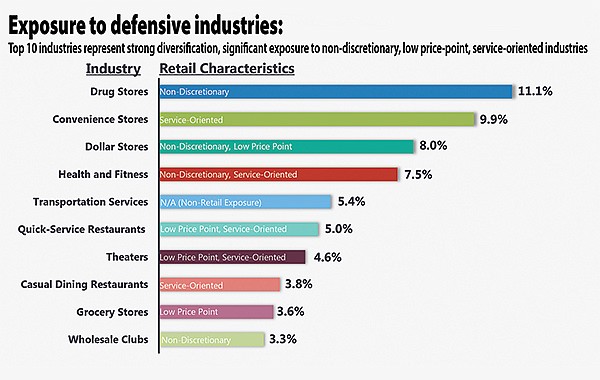

Stores least vulnerable to internet competition.

Australia-based Westfield Corporation has five local malls — UTC, Plaza Bonita, North County, Horton Plaza, and Mission Valley. Westfield UTC, near hyper-upscale La Jolla, has been undergoing an expensive redevelopment since 2012. A second phase of the development will be opened this fall, featuring new cinemas and an expanded food court.

On the other hand, Horton Plaza downtown is a disaster. Important retailers started deserting it not long after it opened. A huge part of it has been ripped down (at taxpayer expense). It has never attracted an upscale clientele, although the Union-Tribune has not stopped referring to it as a great success of public-private projects, or corporate welfare.

Early this year, Macy’s, an anchor of Westfield’s Mission Valley mall, announced it was closing its store at the center. The closure was part of a nationwide shuttering of stores producing unsatisfactory revenue.

“Last year was a terrible year for brick-and-mortar retailers as layoffs and bankruptcies climbed. But 2017 is shaping up to be even worse, particularly for those located in a mall,” says Footnoted.com, a website that combs through companies’ reports to the Securities and Exchange Commission. “Since the start of this year, an alarming number of companies have been making references in their filings to ‘mall traffic.’” Almost always, that is declining mall traffic as a risk factor hurting earnings. The companies that seem to be most afraid of mall-traffic trends are clothing retailers such as Abercrombie & Fitch and food merchants such as Buffalo Wild Wings. (San Diego’s Jack in the Box does not list mall traffic as a risk factor because it has few outlets in malls.)

Now, the battle lines are drawn: it’s the brick-and-mortar retailers versus Amazon or other online operations. A brick-and-mortar retailer losing business to an online merchant is said to be “Amazonned.” The Credit Suisse study forecasts that by 2030 online apparel sales will be 37 percent of the total, more than double today’s percentage.

The companies in the most trouble are the real estate investment trusts that own bundles of shopping malls. Their stocks have been clobbered by 40 percent or more.

There is one real estate investment trust that is sometimes called “Amazon-proof.” It is San Diego’s Realty Income Corp., which, according to Ian Bezek of Investorplace.com, “is arguably the world’s most popular real estate investment trust.” It was founded in 1969 with the purchase of one Taco Bell outlet. Its aim is to produce a steady flow of monthly dividends to investors.

The company is not into malls. It buys freestanding, single-tenant properties, such as a drugstore on a corner. Eighty percent of the properties are in retailing, but the major ones should not be hit by e-commerce. The top ones are Walgreens, 6.8 percent of volume; FedEx, 5.4; Dollar General, 4.1; LA Fitness, 3.8; and Circle K, 2.6. However, “Realty Income’s properties are vulnerable to potential secular shifts within its major industry concentrations,” warns Edward Mui of Morningstar. For example, how will its drugstores react to changes in Washington DC’s proposed new health-care programs? Amazon is considering going into prescription drug delivery. Will folks watch all their movies at home?

Realty Income’s stock climbed to $72.30 last year, greatly because it lacks mall exposure, but has sunk into the mid-$50s this year. Many of its large tenants, such as Walmart and CVS Health Corp., are considered less vulnerable to Amazon. Realty Income has returned 17 percent a year compounded (including dividends) since 1994 and has paid 563 consecutive monthly dividends. That’s great, but, “as the recent news about a potential Amazon Pharmacy reminds us, very little is safe from e-commerce at this point,” says Bezek, and Realty Income’s retailers are brick-and-mortar. Compared to its peers, Realty Income stock is very expensive. Bezek would buy the stock if it gets below $50. Standard & Poor’s has lowered its target for the stock to $62 from $65 and would only hold the stock.

Mergers are muddling the bricks-and-mortar picture. On June 16, Walmart said it will acquire e-commerce apparel retailer Bonobos. The same day, Amazon said it is acquiring Whole Foods. Amazon’s food business has been slow to develop, and now, say analysts, it could soar.

Achilles Research says that Realty Income is “widely seen as the best commercial real estate investment trust thanks to its high quality of earnings,” but despite the company’s splendid historical record, it’s “far from being a bargain,” even though the stock has dropped sharply. The market overall is too high, and stocks paying good dividends are vulnerable. Achilles would also wait until the stock hits $50 to nibble.

Realty Income officials just came back from an analysts’ meeting in New York. The San Diego company feels the drop in its stock is a reflection of rising interest rates. It feels that its top 20 tenants are shielded from online competition. As to Amazon’s rush into the drug business, Realty Income notes that online drug sales peaked at 20 percent of industry sales in 2010 and are now down to 11 percent.

Here's something you might be interested in.

Brick & mortar vs. Amazon

Mall stores getting Amazonned into deep doo-doo

Brick & mortar vs. Amazon

Mall stores getting Amazonned into deep doo-doo

Regal Cinemas — Amazon-proof?

Fifty years ago, shopping malls were the local gathering places. Days and nights, they were jam-packed with people of all demographic groups. But by 2014, almost 20 percent of American malls were considered in trouble — that is, they had vacancy rates of 10 percent or more. It has gotten worse. Deadmalls.com, the website devoted to the topic, says that a dead mall is one having an “occupancy rate in slow or steady decline of 70 percent or less.” And the website lists them by the dozens, although none is in San Diego County.

Horton Plaza. Important retailers started deserting it not long after it opened. A huge part of it has been ripped down.

On May 31, the big bank Credit Suisse predicted that 25 percent of malls would be gone in the next five years. Earlier forecasts had also been dire, and results prove them to have been accurate. Malls used to be anchored by big department stores — Sears, JCPenney, Macy’s, and the like.

San Diego's Realty Investment Corp. success chart. It is not into malls. It buys freestanding, single-tenant properties. (Click to enlarge)

All are now in deep doo-doo and closing stores, upsetting the malls that relied upon them as consumer draws and sources of revenue. The smaller mall stores, which pay higher rent per square foot than the anchors, are having trouble, further biting into mall revenue and traffic.

Much of this is tied to the American economy. For several decades, income growth has gone mainly to the rich and superrich, while the middle class has shrunk. Malls that appeal to the middle and lower-middle classes are hurting. San Diego has a good example of that economically ruinous trend.

Stores least vulnerable to internet competition.

Australia-based Westfield Corporation has five local malls — UTC, Plaza Bonita, North County, Horton Plaza, and Mission Valley. Westfield UTC, near hyper-upscale La Jolla, has been undergoing an expensive redevelopment since 2012. A second phase of the development will be opened this fall, featuring new cinemas and an expanded food court.

On the other hand, Horton Plaza downtown is a disaster. Important retailers started deserting it not long after it opened. A huge part of it has been ripped down (at taxpayer expense). It has never attracted an upscale clientele, although the Union-Tribune has not stopped referring to it as a great success of public-private projects, or corporate welfare.

Early this year, Macy’s, an anchor of Westfield’s Mission Valley mall, announced it was closing its store at the center. The closure was part of a nationwide shuttering of stores producing unsatisfactory revenue.

“Last year was a terrible year for brick-and-mortar retailers as layoffs and bankruptcies climbed. But 2017 is shaping up to be even worse, particularly for those located in a mall,” says Footnoted.com, a website that combs through companies’ reports to the Securities and Exchange Commission. “Since the start of this year, an alarming number of companies have been making references in their filings to ‘mall traffic.’” Almost always, that is declining mall traffic as a risk factor hurting earnings. The companies that seem to be most afraid of mall-traffic trends are clothing retailers such as Abercrombie & Fitch and food merchants such as Buffalo Wild Wings. (San Diego’s Jack in the Box does not list mall traffic as a risk factor because it has few outlets in malls.)

Now, the battle lines are drawn: it’s the brick-and-mortar retailers versus Amazon or other online operations. A brick-and-mortar retailer losing business to an online merchant is said to be “Amazonned.” The Credit Suisse study forecasts that by 2030 online apparel sales will be 37 percent of the total, more than double today’s percentage.

The companies in the most trouble are the real estate investment trusts that own bundles of shopping malls. Their stocks have been clobbered by 40 percent or more.

There is one real estate investment trust that is sometimes called “Amazon-proof.” It is San Diego’s Realty Income Corp., which, according to Ian Bezek of Investorplace.com, “is arguably the world’s most popular real estate investment trust.” It was founded in 1969 with the purchase of one Taco Bell outlet. Its aim is to produce a steady flow of monthly dividends to investors.

The company is not into malls. It buys freestanding, single-tenant properties, such as a drugstore on a corner. Eighty percent of the properties are in retailing, but the major ones should not be hit by e-commerce. The top ones are Walgreens, 6.8 percent of volume; FedEx, 5.4; Dollar General, 4.1; LA Fitness, 3.8; and Circle K, 2.6. However, “Realty Income’s properties are vulnerable to potential secular shifts within its major industry concentrations,” warns Edward Mui of Morningstar. For example, how will its drugstores react to changes in Washington DC’s proposed new health-care programs? Amazon is considering going into prescription drug delivery. Will folks watch all their movies at home?

Realty Income’s stock climbed to $72.30 last year, greatly because it lacks mall exposure, but has sunk into the mid-$50s this year. Many of its large tenants, such as Walmart and CVS Health Corp., are considered less vulnerable to Amazon. Realty Income has returned 17 percent a year compounded (including dividends) since 1994 and has paid 563 consecutive monthly dividends. That’s great, but, “as the recent news about a potential Amazon Pharmacy reminds us, very little is safe from e-commerce at this point,” says Bezek, and Realty Income’s retailers are brick-and-mortar. Compared to its peers, Realty Income stock is very expensive. Bezek would buy the stock if it gets below $50. Standard & Poor’s has lowered its target for the stock to $62 from $65 and would only hold the stock.

Mergers are muddling the bricks-and-mortar picture. On June 16, Walmart said it will acquire e-commerce apparel retailer Bonobos. The same day, Amazon said it is acquiring Whole Foods. Amazon’s food business has been slow to develop, and now, say analysts, it could soar.

Achilles Research says that Realty Income is “widely seen as the best commercial real estate investment trust thanks to its high quality of earnings,” but despite the company’s splendid historical record, it’s “far from being a bargain,” even though the stock has dropped sharply. The market overall is too high, and stocks paying good dividends are vulnerable. Achilles would also wait until the stock hits $50 to nibble.

Realty Income officials just came back from an analysts’ meeting in New York. The San Diego company feels the drop in its stock is a reflection of rising interest rates. It feels that its top 20 tenants are shielded from online competition. As to Amazon’s rush into the drug business, Realty Income notes that online drug sales peaked at 20 percent of industry sales in 2010 and are now down to 11 percent.

Comments