{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Wells Fargo sells credit card terminal to Oceanside swap meet seller

Bank fights small Mexican merchant

This Vista Wells Fargo branch is at the center of a lawsuit alleging deceptive contract practices.

Have you ever been confronted with a nearly inscrutable document and signed or clicked it, only to find that you have agreed to make monthly payments for products or services you have no use for? Or have you failed to read or gotten bewildered in an obfuscated, lengthy document mandating that if you want to sue to get your money back, you will have to file the complaint more than 2000 miles from your home?

I have, but this column is not about me. It’s about Casiano Hernandez-Venegas, a Vista resident who neither speaks nor reads English. He makes $9 an hour at his regular job and has a small part-time business selling used clothing, including at the Oceanside Swap Meet.

Vista resident Casiano Hernandez-Venegas alleges that Wells Fargo had him sign a document they called an application, which was in fact a contract.

According to a lawsuit he filed in North County Superior Court, Hernandez-Venegas banks at a Wells Fargo branch in Vista catering to the Hispanic market. In November of last year, a bank saleswoman was promoting Wells Fargo Merchant Services credit- and debit-card billing-service terminals.

Through an interpreter, the saleswoman asked Hernandez-Venegas if he would like to fill out a three-page “application” to lease a card terminal. According to the suit, he replied that his business is so tiny that his customers pay in cash. The saleslady said it was only an “application” and she would fill out the paperwork. But, he says in the lawsuit, he was not clearly told that the “application” was actually a contract obligating him to make monthly lease payments to a unit of Atlanta-based First Data Corporation for four years.

Hernandez-Venegas let the saleslady fill out the form, believing it was only an application. He was never given a Spanish translation of the document, according to the suit. Pretty soon, a terminal arrived at the bank. Having no use for it, he told Wells Fargo he did not want it.

Beginning in December, Wells Fargo began subtracting around $40 a month for the terminal from Hernandez-Venegas’s account, even though the equipment was still in its box. A lawyer, Conrad Joyner, went to the bank but got no satisfaction. So he filed suit. In July, more than half a year after Hernandez-Venegas first complained, he got his money back. I asked Wells Fargo and First Data a number of questions. I got the same answer from both: “Mr. Hernandez-Venegas was allowed to rescind the merchant account and equipment lease he opened, and received a full refund of all costs and payments associated with those accounts.”

An excerpt from Wells Fargo’s response to the lawsuit.

But shouldn’t Wells Fargo, one of the world’s largest banking institutions, understand the time value of money? A dollar today is worth more than a dollar in the future. The bank and First Data sat on Hernandez-Venegas’s money for months and acted only after he filed suit.

I gave Wells Fargo a chance to say whether or not it denied Hernandez-Venegas’s complaint that he thought he was only signing an application, not a contract. No response. I asked if it wanted to deny that Hernandez-Venegas never got a Spanish translation of what he signed and accompanying materials. No response.

I asked Wells Fargo whether it was a good idea to do business with money-losing and debt-laden First Data. In online scam sites, such as ripoffreport.com, pissedconsumer.com, and consumeraffairs.com, there are numerous complaints about First Data and about how Wells Fargo and First Data collaborate.

Here are some samples: “First Data and Wells Fargo are working together to rip off consumers. I trusted my Wells Fargo banker who didn’t tell me he got a kickback (commission) for signing me up with First Data.… They threatened to ruin my credit if I didn’t pay for the four-year lease.”

Another: A merchant says he was told that he could get out of the First Data contract anytime, but “I am now being told that unless I pay the entire amount of a four-year contract, I cannot be free of First Data and they will continue to charge me for more than another year. The hidden fees are very high.”

Another: “I was duped by Wells Fargo Bank into signing up for merchant services and a 48-month lease.… I called First Data to cancel the lease and they said they could not cancel the lease and that Wells Fargo needs to cancel with First Data.… I have never used the terminal, not once.”

And another: “This is my fault for trusting my bank [Wells Fargo] that I have been with since 1988.”

The complaints go on and on, and many discuss filing a class-action suit. I cannot determine that one has been filed, and neither Wells Fargo nor First Data will answer the question.

You can see from the complaints that these kinds of operations rely on the fact that only a certain percentage of people continue to battle the charges. The squeaky wheels may get some grease, often getting money back, but both Wells Fargo and First Data certainly have a good idea what percentage of people will continue fighting. I asked First Data if it had ever done a study on how many customers actually read the lengthy document handed to them. No response.

In court on August 30, Wells Fargo and First Data will rely on one item interred in a 55-page Program Guide they claim they gave to Hernandez-Venegas. It was in English. Buried inside was a statement that any lawsuits must be heard in Melville, New York, on Long Island, more than 2700 miles from San Diego.

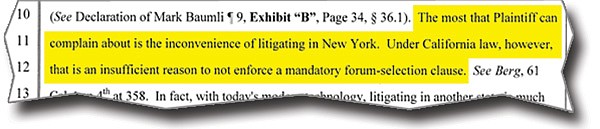

This is called a forum selection clause and is often used to block lawsuits filed by frustrated consumers. Wells Fargo and First Data want Hernandez-Venegas’s suit thrown out. Says their motion — chillingly — “The most that plaintiff can complain about is the inconvenience of litigating in New York. Under California law, however, that is an insufficient reason to not enforce a mandatory forum selection clause.”

Among many things, Joyner will argue that in plenty of cases, Wells Fargo “has no hesitation about ignoring the forum selection clause and suing people here [in California]. It’s a scam.”

If this kind of adventure interests you, there are two books worth reading. One is David Cay Johnston’s The Fine Print: How Big Companies Use “Plain English” to Rob You Blind. Another is Margaret Jane Radin’s Boilerplate: The Fine Print, Vanishing Rights, and the Rule of Law. ■

Contact Don Bauder at 619-546-8529

Here's something you might be interested in.

Wells Fargo sells credit card terminal to Oceanside swap meet seller

Bank fights small Mexican merchant

Wells Fargo sells credit card terminal to Oceanside swap meet seller

Bank fights small Mexican merchant

This Vista Wells Fargo branch is at the center of a lawsuit alleging deceptive contract practices.

Have you ever been confronted with a nearly inscrutable document and signed or clicked it, only to find that you have agreed to make monthly payments for products or services you have no use for? Or have you failed to read or gotten bewildered in an obfuscated, lengthy document mandating that if you want to sue to get your money back, you will have to file the complaint more than 2000 miles from your home?

I have, but this column is not about me. It’s about Casiano Hernandez-Venegas, a Vista resident who neither speaks nor reads English. He makes $9 an hour at his regular job and has a small part-time business selling used clothing, including at the Oceanside Swap Meet.

Vista resident Casiano Hernandez-Venegas alleges that Wells Fargo had him sign a document they called an application, which was in fact a contract.

According to a lawsuit he filed in North County Superior Court, Hernandez-Venegas banks at a Wells Fargo branch in Vista catering to the Hispanic market. In November of last year, a bank saleswoman was promoting Wells Fargo Merchant Services credit- and debit-card billing-service terminals.

Through an interpreter, the saleswoman asked Hernandez-Venegas if he would like to fill out a three-page “application” to lease a card terminal. According to the suit, he replied that his business is so tiny that his customers pay in cash. The saleslady said it was only an “application” and she would fill out the paperwork. But, he says in the lawsuit, he was not clearly told that the “application” was actually a contract obligating him to make monthly lease payments to a unit of Atlanta-based First Data Corporation for four years.

Hernandez-Venegas let the saleslady fill out the form, believing it was only an application. He was never given a Spanish translation of the document, according to the suit. Pretty soon, a terminal arrived at the bank. Having no use for it, he told Wells Fargo he did not want it.

Beginning in December, Wells Fargo began subtracting around $40 a month for the terminal from Hernandez-Venegas’s account, even though the equipment was still in its box. A lawyer, Conrad Joyner, went to the bank but got no satisfaction. So he filed suit. In July, more than half a year after Hernandez-Venegas first complained, he got his money back. I asked Wells Fargo and First Data a number of questions. I got the same answer from both: “Mr. Hernandez-Venegas was allowed to rescind the merchant account and equipment lease he opened, and received a full refund of all costs and payments associated with those accounts.”

An excerpt from Wells Fargo’s response to the lawsuit.

But shouldn’t Wells Fargo, one of the world’s largest banking institutions, understand the time value of money? A dollar today is worth more than a dollar in the future. The bank and First Data sat on Hernandez-Venegas’s money for months and acted only after he filed suit.

I gave Wells Fargo a chance to say whether or not it denied Hernandez-Venegas’s complaint that he thought he was only signing an application, not a contract. No response. I asked if it wanted to deny that Hernandez-Venegas never got a Spanish translation of what he signed and accompanying materials. No response.

I asked Wells Fargo whether it was a good idea to do business with money-losing and debt-laden First Data. In online scam sites, such as ripoffreport.com, pissedconsumer.com, and consumeraffairs.com, there are numerous complaints about First Data and about how Wells Fargo and First Data collaborate.

Here are some samples: “First Data and Wells Fargo are working together to rip off consumers. I trusted my Wells Fargo banker who didn’t tell me he got a kickback (commission) for signing me up with First Data.… They threatened to ruin my credit if I didn’t pay for the four-year lease.”

Another: A merchant says he was told that he could get out of the First Data contract anytime, but “I am now being told that unless I pay the entire amount of a four-year contract, I cannot be free of First Data and they will continue to charge me for more than another year. The hidden fees are very high.”

Another: “I was duped by Wells Fargo Bank into signing up for merchant services and a 48-month lease.… I called First Data to cancel the lease and they said they could not cancel the lease and that Wells Fargo needs to cancel with First Data.… I have never used the terminal, not once.”

And another: “This is my fault for trusting my bank [Wells Fargo] that I have been with since 1988.”

The complaints go on and on, and many discuss filing a class-action suit. I cannot determine that one has been filed, and neither Wells Fargo nor First Data will answer the question.

You can see from the complaints that these kinds of operations rely on the fact that only a certain percentage of people continue to battle the charges. The squeaky wheels may get some grease, often getting money back, but both Wells Fargo and First Data certainly have a good idea what percentage of people will continue fighting. I asked First Data if it had ever done a study on how many customers actually read the lengthy document handed to them. No response.

In court on August 30, Wells Fargo and First Data will rely on one item interred in a 55-page Program Guide they claim they gave to Hernandez-Venegas. It was in English. Buried inside was a statement that any lawsuits must be heard in Melville, New York, on Long Island, more than 2700 miles from San Diego.

This is called a forum selection clause and is often used to block lawsuits filed by frustrated consumers. Wells Fargo and First Data want Hernandez-Venegas’s suit thrown out. Says their motion — chillingly — “The most that plaintiff can complain about is the inconvenience of litigating in New York. Under California law, however, that is an insufficient reason to not enforce a mandatory forum selection clause.”

Among many things, Joyner will argue that in plenty of cases, Wells Fargo “has no hesitation about ignoring the forum selection clause and suing people here [in California]. It’s a scam.”

If this kind of adventure interests you, there are two books worth reading. One is David Cay Johnston’s The Fine Print: How Big Companies Use “Plain English” to Rob You Blind. Another is Margaret Jane Radin’s Boilerplate: The Fine Print, Vanishing Rights, and the Rule of Law. ■

Contact Don Bauder at 619-546-8529

Comments