{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Lou Schooler and John Schooler's dubious schemes

The fine print prevails

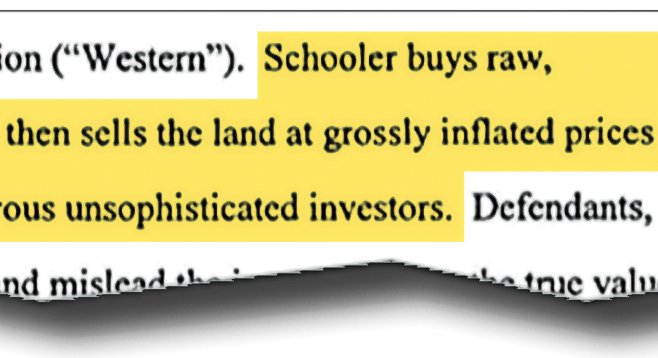

This excerpt from the Securities & Exchange Commission’s complaint against Lou Schooler lists one of the fraudulent practices in which the Schooler brothers engaged.

San Diegans wanting to entrust their money to glib securities peddlers can go to school on the Schoolers — Lou and John Schooler. Lou owns Western Financial Planning Corporation, which has been charged with running a $50 million real estate fraud. Lou indirectly owns half of a brokerage house called WFP Securities, run by his brother John, who has a smaller ownership position in the web of Schooler-dominated firms. The WFP brokerage house put elderly, financially squeezed investors in dubious investment schemes, some later deemed fraudulent by the government. In an April column last year, I showed how the brokerage house was drowning in arbitration claims from indignant investors. It closed its doors two months later.

John Schooler ran WFP Securities, which put elderly, financially squeezed investors in dubious schemes.

The brokerage house now exists mainly to settle the arbitrations — generally for low amounts because “you can’t get blood from a stone,” says Miami attorney Jeffrey Kaplan, who handled several arbitrations. The brokerage house “didn’t have adequate insurance and has no money. A lot of the products sold by WFP Securities were risky, illiquid, high-commission products. The driving force was brokers’ desire to get high commissions.”

Lou Schooler’s company stands charged with making fraudulent land deals.

WFP brokers also sold Western Financial real estate deals. The Securities and Exchange Commission in September charged that since 2007, Lou Schooler and Western Financial have been defrauding investors in land partnerships. “Schooler buys raw, undeveloped land in the southwest United States, then sells the land at grossly inflated prices to general partnerships comprised of numerous unsophisticated investors,” says the securities agency. But Western Financial doesn’t disclose the “enormous markup” to investors, according to the government.

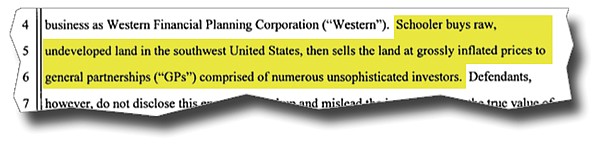

This excerpt from the Securities & Exchange Commission’s complaint against Lou Schooler lists one of the fraudulent practices in which the Schooler brothers engaged.

For example, Western Financial is now offering Nevada land that it purchased for $1.85 million two years ago. Western has sold chunks of that land to investors for a total of $9.3 million — about a 500 percent markup, says the agency. In addition, Western woos investors by quoting the values of so-called comparable pieces of land (called “comps”) that aren’t comparable at all, says the agency.

Last year, after some not-so-unsophisticated investors figured out the alleged scam, Schooler returned their money in exchange for a promise to keep quiet; the government agency calls it “hush money.”

A federal judge temporarily froze Western Financial’s assets, named a receiver, and banned any document destruction. On October 5, the judge ruled that there is a prima facie case that the defendants violated securities laws. He said the securities agency has offered no evidence that defendants are hiding or sheltering money, he was not impressed with the “hush money” assertion, and he thought the argument for a further asset freeze was tenuous. Nonetheless, Schooler agreed to a continuation of the freeze. No more land deals are being sold now.

San Diego attorney Ron Marron had three clients who lost money in WFP Securities; two also lost in Western Financial. After getting settlements last year, “they are satisfied,” says Marron. He says that the brokerage house and Western Financial Planning are essentially the same entity, controlled by Lou and John Schooler. “They are alter egos aiding and abetting each other.”

In August of 2011, one San Diegan, having read my piece on WFP, called me about Western Financial. He figured that he and fellow investors had paid far too much for the land in one of Western Financial’s deals. “It will take forever for us to get back the money we paid,” he said at the time. He won’t discuss the matter now.

John Schooler is back in the securities business with a Scottsdale firm. His Financial Industry Regulatory Authority records show 14 complaints and arbitrations. Most of the settlements are wee: for example, alleged damages of $250,000 and a settlement of $15,000, and alleged damages of $335,000 and a settlement of $42,500. His Los Angeles attorney Brandon Reif concedes that the settlement amounts are low.

“Just because investments decline in value or there are allegations of wrongdoing at the sponsor level, it does not translate into misconduct at the securities firm,” Reif claims. Those who got skinned in those brokerage-house deals — which included Ponzi schemes — argue vehemently that the brokerage house did not do its due diligence and sold risky deals that were hardly appropriate for those wanting conservative income.

Reif argues that there are “significant risks inherent in investing in private or publicly non-traded investments…new business ventures do not have audited financials.” Ergo, due diligence is difficult. He says the investors knew the risks.

Hmm. Take the case of Orange County’s Jaimie Davis. She lost $2.3 million in speculative WFP securities, lost her arbitration before the Financial Industry Regulatory Authority, and had to forfeit $135,000 to WFP and related parties for costs. She had gone into arbitration against the issuers of the bum securities before a competing dispute-resolution panel, Judicial Arbitration and Mediation Services. That’s a no-no with the regulatory authority, and its arbitration panel dinged her. Davis’s lawyer, Sacramento’s Melinda Jane Steuer, says Davis wouldn’t have taken settlements from two sides in the same dispute.

Davis is appealing on the grounds that the arbitration panel excluded her sole expert from testifying. Also, WFP intimidated a witness from testifying, according to sworn statements by both the frightened potential witness and Davis’s then attorney. Reif says those declarations were false.

One ruling in Davis’s case was poignant. Her broker told her an investment was safe. But she admitted she had read a document that told of risk factors. The panel cited a precedent from another case: “If a literate, competent adult is given a document that in readable and comprehensive prose says X (X might be, ‘this is a risky investment’) and the person who hands it to him tells him, orally, not-X (‘this is a safe investment’), our literate competent adult cannot maintain an action of fraud.”

In other words, if a smarmy broker tells you an untruth, but the fine print says otherwise, the fine print prevails.

Since WFP and Western Financial are joined at the hip, the big question is why hasn’t the securities commission added the brokerage house to the case? Neither the commission nor the receiver responded to that question. ■

Here's something you might be interested in.

Lou Schooler and John Schooler's dubious schemes

The fine print prevails

Lou Schooler and John Schooler's dubious schemes

The fine print prevails

This excerpt from the Securities & Exchange Commission’s complaint against Lou Schooler lists one of the fraudulent practices in which the Schooler brothers engaged.

San Diegans wanting to entrust their money to glib securities peddlers can go to school on the Schoolers — Lou and John Schooler. Lou owns Western Financial Planning Corporation, which has been charged with running a $50 million real estate fraud. Lou indirectly owns half of a brokerage house called WFP Securities, run by his brother John, who has a smaller ownership position in the web of Schooler-dominated firms. The WFP brokerage house put elderly, financially squeezed investors in dubious investment schemes, some later deemed fraudulent by the government. In an April column last year, I showed how the brokerage house was drowning in arbitration claims from indignant investors. It closed its doors two months later.

John Schooler ran WFP Securities, which put elderly, financially squeezed investors in dubious schemes.

The brokerage house now exists mainly to settle the arbitrations — generally for low amounts because “you can’t get blood from a stone,” says Miami attorney Jeffrey Kaplan, who handled several arbitrations. The brokerage house “didn’t have adequate insurance and has no money. A lot of the products sold by WFP Securities were risky, illiquid, high-commission products. The driving force was brokers’ desire to get high commissions.”

Lou Schooler’s company stands charged with making fraudulent land deals.

WFP brokers also sold Western Financial real estate deals. The Securities and Exchange Commission in September charged that since 2007, Lou Schooler and Western Financial have been defrauding investors in land partnerships. “Schooler buys raw, undeveloped land in the southwest United States, then sells the land at grossly inflated prices to general partnerships comprised of numerous unsophisticated investors,” says the securities agency. But Western Financial doesn’t disclose the “enormous markup” to investors, according to the government.

This excerpt from the Securities & Exchange Commission’s complaint against Lou Schooler lists one of the fraudulent practices in which the Schooler brothers engaged.

For example, Western Financial is now offering Nevada land that it purchased for $1.85 million two years ago. Western has sold chunks of that land to investors for a total of $9.3 million — about a 500 percent markup, says the agency. In addition, Western woos investors by quoting the values of so-called comparable pieces of land (called “comps”) that aren’t comparable at all, says the agency.

Last year, after some not-so-unsophisticated investors figured out the alleged scam, Schooler returned their money in exchange for a promise to keep quiet; the government agency calls it “hush money.”

A federal judge temporarily froze Western Financial’s assets, named a receiver, and banned any document destruction. On October 5, the judge ruled that there is a prima facie case that the defendants violated securities laws. He said the securities agency has offered no evidence that defendants are hiding or sheltering money, he was not impressed with the “hush money” assertion, and he thought the argument for a further asset freeze was tenuous. Nonetheless, Schooler agreed to a continuation of the freeze. No more land deals are being sold now.

San Diego attorney Ron Marron had three clients who lost money in WFP Securities; two also lost in Western Financial. After getting settlements last year, “they are satisfied,” says Marron. He says that the brokerage house and Western Financial Planning are essentially the same entity, controlled by Lou and John Schooler. “They are alter egos aiding and abetting each other.”

In August of 2011, one San Diegan, having read my piece on WFP, called me about Western Financial. He figured that he and fellow investors had paid far too much for the land in one of Western Financial’s deals. “It will take forever for us to get back the money we paid,” he said at the time. He won’t discuss the matter now.

John Schooler is back in the securities business with a Scottsdale firm. His Financial Industry Regulatory Authority records show 14 complaints and arbitrations. Most of the settlements are wee: for example, alleged damages of $250,000 and a settlement of $15,000, and alleged damages of $335,000 and a settlement of $42,500. His Los Angeles attorney Brandon Reif concedes that the settlement amounts are low.

“Just because investments decline in value or there are allegations of wrongdoing at the sponsor level, it does not translate into misconduct at the securities firm,” Reif claims. Those who got skinned in those brokerage-house deals — which included Ponzi schemes — argue vehemently that the brokerage house did not do its due diligence and sold risky deals that were hardly appropriate for those wanting conservative income.

Reif argues that there are “significant risks inherent in investing in private or publicly non-traded investments…new business ventures do not have audited financials.” Ergo, due diligence is difficult. He says the investors knew the risks.

Hmm. Take the case of Orange County’s Jaimie Davis. She lost $2.3 million in speculative WFP securities, lost her arbitration before the Financial Industry Regulatory Authority, and had to forfeit $135,000 to WFP and related parties for costs. She had gone into arbitration against the issuers of the bum securities before a competing dispute-resolution panel, Judicial Arbitration and Mediation Services. That’s a no-no with the regulatory authority, and its arbitration panel dinged her. Davis’s lawyer, Sacramento’s Melinda Jane Steuer, says Davis wouldn’t have taken settlements from two sides in the same dispute.

Davis is appealing on the grounds that the arbitration panel excluded her sole expert from testifying. Also, WFP intimidated a witness from testifying, according to sworn statements by both the frightened potential witness and Davis’s then attorney. Reif says those declarations were false.

One ruling in Davis’s case was poignant. Her broker told her an investment was safe. But she admitted she had read a document that told of risk factors. The panel cited a precedent from another case: “If a literate, competent adult is given a document that in readable and comprehensive prose says X (X might be, ‘this is a risky investment’) and the person who hands it to him tells him, orally, not-X (‘this is a safe investment’), our literate competent adult cannot maintain an action of fraud.”

In other words, if a smarmy broker tells you an untruth, but the fine print says otherwise, the fine print prevails.

Since WFP and Western Financial are joined at the hip, the big question is why hasn’t the securities commission added the brokerage house to the case? Neither the commission nor the receiver responded to that question. ■

Comments