{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Economy for 2013: San Diego worse than state, nation?

Ross Starr: Spending is sluggish

Are you tired of sluggish economic growth? Well, you could live in Europe, which is in a recession, or Japan, which has been struggling since 1989. Local economists look for slow growth in the United States, California, and San Diego next year, amid continuing global woes — and maybe even a sharp slowdown in booming China.

Problem: our slow growth won’t be good enough to improve our festering unemployment problem significantly. Our central bank, the Federal Reserve, will continue to drive interest rates lower, supposedly to combat joblessness. This could make Wall Street happier, as stock and bond prices rise with more money floating around, but won’t help Main Street much except in one important way: housing could continue its rebound.

Ross Starr, professor of economics at the University of California San Diego, says the United States economy will grow by about 2 percent, although inability to fix fiscal cliff problems could have us in a recession by midyear. Europe “could hit bottom, but will be recovering from an immensely depressed level,” says Starr. “Japan is in stagnation but may be perking up.” Both Europe and Japan need cheaper currencies, but there are institutional roadblocks. “China has had immensely rapid growth,” but its attempt to transition from an investment to a consumption economy could slow it down sharply.

James Hamiltion: Growth will be sluggish

Kelly Cunningham: San Diego economy will be sluggish

In the United States, both consumer and capital spending have been slowed down by uncertainty about taxes and government spending. Happily, “the remarkably low long-term interest rates” engineered by the Federal Reserve will prop up housing, which has been a drag for years, says Starr.

“In the U.S., the sluggish growth of the last three years is a reasonable forecast for 2013,” says James Hamilton, professor of economics at the University of California San Diego. He thinks the economy could grow by possibly 2.5 percent, but he warns that to create jobs growth “we need in excess of 2.5 percent before we could say we have turned the corner.” He is concerned about declining consumer confidence.

Both Kelly Cunningham, economist for the National University System Institute for Policy Research, and Marney Cox, chief economist for the San Diego Association of Governments, look for a sluggish San Diego economy next year. The military — including personnel as well as contracting — has accounted for as much as 25 percent of the economy in recent years, but that’s coming down and could drop almost to 20 percent, says Cunningham.

“Starting in the fourth quarter of this year, there have been military declines; some contractors have sent out notices of layoffs,” says Cox. The biggest impact thus far has been in contracting, but “we could lose 10,000 to 20,000 uniformed military personnel, mostly in the Marine Corps, in 2013,” says Cox. “This could possibly be offset by the shift of the military from the East Coast to the West Coast.”

San Diego’s Northrop Grumman and General Atomics Aeronautical Systems are the nation’s big builders of drones. There are rumors of possible drone cutbacks — but also rumors of expansion of that business.

Cox thinks the county will add only 12,000 jobs next year — a 1 percent gain over 2012, when the same number of jobs was added. There will be declines in local government employment but stabilization in state government jobs. There should be more teacher openings. Healthcare employment will do well, as usual. “One of the places we will see employment growth is in construction,” says Cox, as residential business picks up. Home values will probably rise 5 percent, greatly because of the low interest rates. (Keep in mind that home values plunged by more than 40 percent beginning in late 2005 and are still down by about 35 percent from that peak. Median home values are above $360,000, among the highest in the nation.)

In its heyday, real estate, including construction, represented 23 percent of the San Diego economy, says Cunningham. Only a couple of sizzling Florida markets had higher percentages. San Diego’s percentage has gone down, says Cunningham.

In 2013, “consumer spending will slow,” says Cunningham. Higher taxes will definitely impact spending. Coming out of the 2008–2009 debacle, “we were showing consumer-spending increases, but on a per capita basis we are far below where we were before.” One problem is that internet purchases haven’t been counted in taxable sales. But that began changing in September, when Amazon.com, the biggest online merchant, started collecting sales taxes on purchases made by California buyers. Those tax receipts will help local governments. But whether sales are brick-and-mortar or online, “people are just not spending,” and the tightfistedness may intensify next year.

“There is not much income growth,” says Cox. “There are more people with jobs, but they are not earning as much.” On the other hand, some are doing very well — particularly in tech. Investment capital is pouring into San Diego far more rapidly than in recent years, notes Cox. A December report by the Bay Area Council Economic Institute indicates that tech jobs are 11.1 percent of San Diego County jobs. That puts the metro area 13th in the nation. The average San Diego tech salary is $110,408, topping the United States average of $95,832.

Tourism is recovering, says Cox, but employment is not back up to pre-recession levels. Travel expert Jerry Morrison of Encinitas notes that the San Diego occupancy rate and average daily room rate still lag comparable 2007 levels. But San Francisco, Los Angeles, and Orange County have done much better recovering.

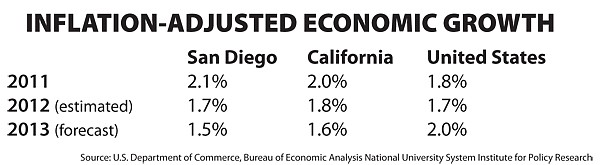

In 2011, the San Diego economy grew by 2.1 percent adjusted for inflation. This year, it will grow by 1.7 percent. Next year? Even lower — 1.5 percent, says Cunningham. That would be worse than California’s 1.6 percent and the nation’s 2 percent. Cox thinks San Diego’s inflation-adjusted growth could be 2 to 2.5 percent, but the gain would largely be coming from productivity, or output per worker hour.

So you may be told to do more work for the same amount of pay — or less. ■

Contact Don Bauder at 619-546-8529

Here's something you might be interested in.

Economy for 2013: San Diego worse than state, nation?

Economy for 2013: San Diego worse than state, nation?

Ross Starr: Spending is sluggish

Are you tired of sluggish economic growth? Well, you could live in Europe, which is in a recession, or Japan, which has been struggling since 1989. Local economists look for slow growth in the United States, California, and San Diego next year, amid continuing global woes — and maybe even a sharp slowdown in booming China.

Problem: our slow growth won’t be good enough to improve our festering unemployment problem significantly. Our central bank, the Federal Reserve, will continue to drive interest rates lower, supposedly to combat joblessness. This could make Wall Street happier, as stock and bond prices rise with more money floating around, but won’t help Main Street much except in one important way: housing could continue its rebound.

Ross Starr, professor of economics at the University of California San Diego, says the United States economy will grow by about 2 percent, although inability to fix fiscal cliff problems could have us in a recession by midyear. Europe “could hit bottom, but will be recovering from an immensely depressed level,” says Starr. “Japan is in stagnation but may be perking up.” Both Europe and Japan need cheaper currencies, but there are institutional roadblocks. “China has had immensely rapid growth,” but its attempt to transition from an investment to a consumption economy could slow it down sharply.

James Hamiltion: Growth will be sluggish

Kelly Cunningham: San Diego economy will be sluggish

In the United States, both consumer and capital spending have been slowed down by uncertainty about taxes and government spending. Happily, “the remarkably low long-term interest rates” engineered by the Federal Reserve will prop up housing, which has been a drag for years, says Starr.

“In the U.S., the sluggish growth of the last three years is a reasonable forecast for 2013,” says James Hamilton, professor of economics at the University of California San Diego. He thinks the economy could grow by possibly 2.5 percent, but he warns that to create jobs growth “we need in excess of 2.5 percent before we could say we have turned the corner.” He is concerned about declining consumer confidence.

Both Kelly Cunningham, economist for the National University System Institute for Policy Research, and Marney Cox, chief economist for the San Diego Association of Governments, look for a sluggish San Diego economy next year. The military — including personnel as well as contracting — has accounted for as much as 25 percent of the economy in recent years, but that’s coming down and could drop almost to 20 percent, says Cunningham.

“Starting in the fourth quarter of this year, there have been military declines; some contractors have sent out notices of layoffs,” says Cox. The biggest impact thus far has been in contracting, but “we could lose 10,000 to 20,000 uniformed military personnel, mostly in the Marine Corps, in 2013,” says Cox. “This could possibly be offset by the shift of the military from the East Coast to the West Coast.”

San Diego’s Northrop Grumman and General Atomics Aeronautical Systems are the nation’s big builders of drones. There are rumors of possible drone cutbacks — but also rumors of expansion of that business.

Cox thinks the county will add only 12,000 jobs next year — a 1 percent gain over 2012, when the same number of jobs was added. There will be declines in local government employment but stabilization in state government jobs. There should be more teacher openings. Healthcare employment will do well, as usual. “One of the places we will see employment growth is in construction,” says Cox, as residential business picks up. Home values will probably rise 5 percent, greatly because of the low interest rates. (Keep in mind that home values plunged by more than 40 percent beginning in late 2005 and are still down by about 35 percent from that peak. Median home values are above $360,000, among the highest in the nation.)

In its heyday, real estate, including construction, represented 23 percent of the San Diego economy, says Cunningham. Only a couple of sizzling Florida markets had higher percentages. San Diego’s percentage has gone down, says Cunningham.

In 2013, “consumer spending will slow,” says Cunningham. Higher taxes will definitely impact spending. Coming out of the 2008–2009 debacle, “we were showing consumer-spending increases, but on a per capita basis we are far below where we were before.” One problem is that internet purchases haven’t been counted in taxable sales. But that began changing in September, when Amazon.com, the biggest online merchant, started collecting sales taxes on purchases made by California buyers. Those tax receipts will help local governments. But whether sales are brick-and-mortar or online, “people are just not spending,” and the tightfistedness may intensify next year.

“There is not much income growth,” says Cox. “There are more people with jobs, but they are not earning as much.” On the other hand, some are doing very well — particularly in tech. Investment capital is pouring into San Diego far more rapidly than in recent years, notes Cox. A December report by the Bay Area Council Economic Institute indicates that tech jobs are 11.1 percent of San Diego County jobs. That puts the metro area 13th in the nation. The average San Diego tech salary is $110,408, topping the United States average of $95,832.

Tourism is recovering, says Cox, but employment is not back up to pre-recession levels. Travel expert Jerry Morrison of Encinitas notes that the San Diego occupancy rate and average daily room rate still lag comparable 2007 levels. But San Francisco, Los Angeles, and Orange County have done much better recovering.

In 2011, the San Diego economy grew by 2.1 percent adjusted for inflation. This year, it will grow by 1.7 percent. Next year? Even lower — 1.5 percent, says Cunningham. That would be worse than California’s 1.6 percent and the nation’s 2 percent. Cox thinks San Diego’s inflation-adjusted growth could be 2 to 2.5 percent, but the gain would largely be coming from productivity, or output per worker hour.

So you may be told to do more work for the same amount of pay — or less. ■

Contact Don Bauder at 619-546-8529

Comments