{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Who caused San Diego's massive power failure September 8?

SDG&E blames utility worker at Arizona Public Service

SDG&E and Arizona Public Service tried to blame the September 8 blackout on a single worker. Critics reject the explanation.

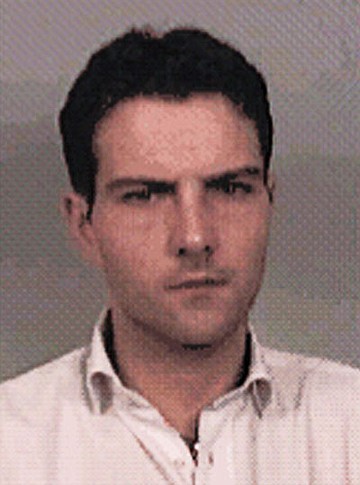

Fumbling European banks may drag the whole world into another slough, but a couple of them have done the right things responding to adversity. A trader at UBS (once known as Union Bank of Switzerland) recently lost $2.3 billion on a bunch of bad bets, tried to cover them up with phony trades, and finally turned himself in. He was immediately branded a rogue trader — losing all that money on his own, without management’s permission or knowledge.

Trader Kweku Adoboli lost $2.3 billion for UBS.

The trader, Kweku Adoboli, has confessed his sins and gone to the slammer. Then something refreshing happened: the bank’s chief executive, an icon in European banking circles, resigned. “As [chief executive officer] I bear full responsibility for what occurs at UBS,” he declared. Good. Management is admitting it lacks a failsafe system that will thwart out-of-control individuals, and the top head is rolling.

Rogue trader Jérôme Kerviel became a folk hero.

Then there was Jérôme Kerviel, a trader for France’s Société Générale, who allegedly lost $6.7 billion for the bank, exceeding his trading limits by a mile. The trades were discovered in 2008. Like Adoboli, Kerviel was allegedly making unauthorized trades and then creating phony transactions to cover up the transgressions. This bank, too, admitted its own failures and weaknesses in its risk control system. The institution fired Kerviel’s two direct supervisors. The bank’s three top officials, including the chief executive officer, volunteered to resign, but the board asked them to stay. However, the chief executive soon stepped down.

The main point is this: so-called rogues, or individuals allegedly acting alone, don’t bring a well-managed company to its knees. Trying to blame one person for a huge loss is an admission that the company does not have adequate risk control systems. In the investment world, traders are encouraged to take big gambles. When they backfire, one trader is often blamed. (Although Kerviel has been sentenced to prison, he is a folk hero in France, where people recognize that the blame game is phony.) It’s similar with shock jocks: they are paid to be outrageous, but when they step too far over the line, offending a key constituency, management saws off the limb they are perched upon.

In an intelligently managed company, when the company’s reputation or billions of dollars are at stake, no one person’s neck should ever be in a noose.

Are you listening, San Diego Gas & Electric? Are you listening, Arizona Public Service? There was a massive power failure September 8 that knocked out San Diego and Imperial counties and parts of Orange County, Arizona, and Mexico. Initially, the blame was heaped on one forlorn Arizona Public Service laborer in the North Gila substation in Yuma County. He supposedly was responsible for a short that caused the transmission line that carries power into California to disconnect, causing the dominoes to fall and leaving millions of people in the dark.

Michael Shames, executive director of Utility Consumers’ Action Network (UCAN), scoffing at this tale, wrote Michael Niggli, chief operating officer of San Diego Gas, and requested data that would authenticate the claim that a single worker was responsible for the blackout. Shames calls that alibi the “Homer Simpson” theory.

Niggli had a lawyer write a letter to Shames. It said that the Federal Energy Regulatory Commission and the North American Electric Reliability Corporation were making an inquiry into the blackout. San Diego Gas “will respond only to government entities involved in the investigation,” said the letter. “Responding to data requests from non-governmental entities would inappropriately divert resources away from the formal investigation and would only serve to confuse the public,” stated the lawyer’s missive.

Hmm… “Now that [San Diego Gas] has bamboozled the public into thinking that a single utility worker at Arizona Public Service caused the massive power failure of September 8, 2011, it now wants to avoid any further confusion that might lead the public into thinking about the real story,” wrote UCAN’s Charles Langley on the watchdog’s website. “And the real story, as it will turn out, had little to do with the poor Arizona worker. It took a lot of people and a lot of wrong decisions” to take down reactors at the San Onofre nuclear power plant and collapse the power grid.

One purported rogue case affecting many San Diegans is still working its way through the legal maze. Five years ago, the San Diego County Employees Retirement Association, which serves county retirees, boasted incessantly about its strategies to bring in fat returns year after year. At that time, the association had 20 percent of its portfolio in hedge funds, those high-risk pools of private capital that are often run by billionaires, sometimes from offshore tax hideaways.

The county association had $175 million invested with Amaranth Advisors, a hedge fund that closed down — not surprisingly, because it lost $6.6 billion of its $9 billion portfolio betting the wrong way on natural gas futures contracts. One young fellow, a Canadian named Brian Hunter, got the blame. The Commodity Futures Trading Commission and the Federal Energy Regulatory Commission accused Hunter and Amaranth of manipulating gas prices. They wanted to levy a $291 million fine on Amaranth, but eventually that was whittled down to $7.5 million.

The Senate Permanent Subcommittee on Investigations issued a 130-page report charging that Amaranth’s manipulations caused huge price swings in the natural gas market and ultimately socked consumers with higher prices. The Federal Energy Regulatory Commission fined Hunter $30 million, but among other things, he said the agency had no authority because he is a Canadian citizen.

The retirement association had $175 million invested with Amaranth. It got $84.9 million back and sued Amaranth, Hunter, and three of Amaranth’s officials, including the chief risk officer for the balance. In 2007, when the suit was filed, the retirement association’s chairman charged that Amaranth “turned our money over to Mr. Hunter, who in my opinion was an absentee rookie trader located thousands of miles from Amaranth’s office.” Then, Amaranth “recklessly failed to apply even basic risk management techniques and controls” to monitor Hunter, according to the suit. However, a New York court ruled last year that Amaranth had warned investors that they could lose all their money. The retirement association lost at the trial level. The suit is now on appeal. The association still entrusts its money to hedge funds but in a more balanced way.

“Don’t put all your eggs in one basket,” says an old adage. But those who do put too many eggs in one basket — say, in the hands of one person — better watch that basket intently. Blaming one individual is a sure sign of incompetence and disingenuousness.

Here's something you might be interested in.

Who caused San Diego's massive power failure September 8?

SDG&E blames utility worker at Arizona Public Service

Who caused San Diego's massive power failure September 8?

SDG&E blames utility worker at Arizona Public Service

SDG&E and Arizona Public Service tried to blame the September 8 blackout on a single worker. Critics reject the explanation.

Fumbling European banks may drag the whole world into another slough, but a couple of them have done the right things responding to adversity. A trader at UBS (once known as Union Bank of Switzerland) recently lost $2.3 billion on a bunch of bad bets, tried to cover them up with phony trades, and finally turned himself in. He was immediately branded a rogue trader — losing all that money on his own, without management’s permission or knowledge.

Trader Kweku Adoboli lost $2.3 billion for UBS.

The trader, Kweku Adoboli, has confessed his sins and gone to the slammer. Then something refreshing happened: the bank’s chief executive, an icon in European banking circles, resigned. “As [chief executive officer] I bear full responsibility for what occurs at UBS,” he declared. Good. Management is admitting it lacks a failsafe system that will thwart out-of-control individuals, and the top head is rolling.

Rogue trader Jérôme Kerviel became a folk hero.

Then there was Jérôme Kerviel, a trader for France’s Société Générale, who allegedly lost $6.7 billion for the bank, exceeding his trading limits by a mile. The trades were discovered in 2008. Like Adoboli, Kerviel was allegedly making unauthorized trades and then creating phony transactions to cover up the transgressions. This bank, too, admitted its own failures and weaknesses in its risk control system. The institution fired Kerviel’s two direct supervisors. The bank’s three top officials, including the chief executive officer, volunteered to resign, but the board asked them to stay. However, the chief executive soon stepped down.

The main point is this: so-called rogues, or individuals allegedly acting alone, don’t bring a well-managed company to its knees. Trying to blame one person for a huge loss is an admission that the company does not have adequate risk control systems. In the investment world, traders are encouraged to take big gambles. When they backfire, one trader is often blamed. (Although Kerviel has been sentenced to prison, he is a folk hero in France, where people recognize that the blame game is phony.) It’s similar with shock jocks: they are paid to be outrageous, but when they step too far over the line, offending a key constituency, management saws off the limb they are perched upon.

In an intelligently managed company, when the company’s reputation or billions of dollars are at stake, no one person’s neck should ever be in a noose.

Are you listening, San Diego Gas & Electric? Are you listening, Arizona Public Service? There was a massive power failure September 8 that knocked out San Diego and Imperial counties and parts of Orange County, Arizona, and Mexico. Initially, the blame was heaped on one forlorn Arizona Public Service laborer in the North Gila substation in Yuma County. He supposedly was responsible for a short that caused the transmission line that carries power into California to disconnect, causing the dominoes to fall and leaving millions of people in the dark.

Michael Shames, executive director of Utility Consumers’ Action Network (UCAN), scoffing at this tale, wrote Michael Niggli, chief operating officer of San Diego Gas, and requested data that would authenticate the claim that a single worker was responsible for the blackout. Shames calls that alibi the “Homer Simpson” theory.

Niggli had a lawyer write a letter to Shames. It said that the Federal Energy Regulatory Commission and the North American Electric Reliability Corporation were making an inquiry into the blackout. San Diego Gas “will respond only to government entities involved in the investigation,” said the letter. “Responding to data requests from non-governmental entities would inappropriately divert resources away from the formal investigation and would only serve to confuse the public,” stated the lawyer’s missive.

Hmm… “Now that [San Diego Gas] has bamboozled the public into thinking that a single utility worker at Arizona Public Service caused the massive power failure of September 8, 2011, it now wants to avoid any further confusion that might lead the public into thinking about the real story,” wrote UCAN’s Charles Langley on the watchdog’s website. “And the real story, as it will turn out, had little to do with the poor Arizona worker. It took a lot of people and a lot of wrong decisions” to take down reactors at the San Onofre nuclear power plant and collapse the power grid.

One purported rogue case affecting many San Diegans is still working its way through the legal maze. Five years ago, the San Diego County Employees Retirement Association, which serves county retirees, boasted incessantly about its strategies to bring in fat returns year after year. At that time, the association had 20 percent of its portfolio in hedge funds, those high-risk pools of private capital that are often run by billionaires, sometimes from offshore tax hideaways.

The county association had $175 million invested with Amaranth Advisors, a hedge fund that closed down — not surprisingly, because it lost $6.6 billion of its $9 billion portfolio betting the wrong way on natural gas futures contracts. One young fellow, a Canadian named Brian Hunter, got the blame. The Commodity Futures Trading Commission and the Federal Energy Regulatory Commission accused Hunter and Amaranth of manipulating gas prices. They wanted to levy a $291 million fine on Amaranth, but eventually that was whittled down to $7.5 million.

The Senate Permanent Subcommittee on Investigations issued a 130-page report charging that Amaranth’s manipulations caused huge price swings in the natural gas market and ultimately socked consumers with higher prices. The Federal Energy Regulatory Commission fined Hunter $30 million, but among other things, he said the agency had no authority because he is a Canadian citizen.

The retirement association had $175 million invested with Amaranth. It got $84.9 million back and sued Amaranth, Hunter, and three of Amaranth’s officials, including the chief risk officer for the balance. In 2007, when the suit was filed, the retirement association’s chairman charged that Amaranth “turned our money over to Mr. Hunter, who in my opinion was an absentee rookie trader located thousands of miles from Amaranth’s office.” Then, Amaranth “recklessly failed to apply even basic risk management techniques and controls” to monitor Hunter, according to the suit. However, a New York court ruled last year that Amaranth had warned investors that they could lose all their money. The retirement association lost at the trial level. The suit is now on appeal. The association still entrusts its money to hedge funds but in a more balanced way.

“Don’t put all your eggs in one basket,” says an old adage. But those who do put too many eggs in one basket — say, in the hands of one person — better watch that basket intently. Blaming one individual is a sure sign of incompetence and disingenuousness.

Comments