{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

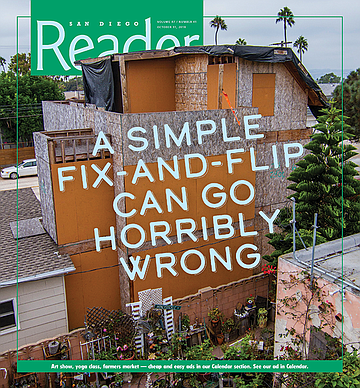

A simple fix-and-flip can go horribly wrong

Will this part of Ebers Street ever be the same?

A long-derided construction project at 2269 Ebers Street in Ocean Beach, spearheaded by Curtis Nelson of Nelco Properties, officially suffered its death blow this spring; after failing to attract a buyer at a foreclosure auction, ownership of the property reverted to Center Street Lending, an Irvine-based hard money lender that specializes in providing financing to “property flippers” seeking to buy low, complete a quick remodel, and resell properties at a significant profit.

Nelco’s ownership of the property – two short blocks off West Point Loma Boulevard and a block east of Sunset Cliffs Boulevard – was frequently controversial — at times the developer bragged on social media about his disregard for the coastal height limit, advertised his development as a two-unit property (it was permitted for only one residence), and drew fire from the community for allowing the property to fall into disrepair after illegal construction was halted by the city. But a dive into the financial history of the property offers an interesting look at how a simple fix-and-flip deal can go horribly wrong.

The original four-bedroom, two-bath home (right) and the expansion.

Nelco originally bought the four-bedroom, two-bath fixer for $645,000 in mid-2015. The home, built in 1927, sits about five blocks from Dog Beach and nine blocks from Newport Avenue, OB’s main drag. Residents here tend to be quieter and more entrenched in the OB lifestyle than the younger, more transient denizens of the neighborhood to the west locals refer to as the “war zone.”

Frank Gormlie’s OB Rag news blog drew attention to the illegal construction

San Diego’s multiple listing service indicates the home was paid for with cash, but that cash wasn’t necessarily Nelco’s. On the same day the sale was finalized, three separate loans were recorded against the property for a total of $949,000 — a full $304,000 more than the purchase price.

Experienced developers are often able to leverage other people’s money to fund their projects. That money, though, often comes at a high cost in the form of interest rates of 10 percent or more, compared to common conventional rates in the mid-4 percent range. Still, borrowing 147 percent of a home’s sale price is approaching exceptional, and we’re just getting started.

About 50 OB residents gathered to protest the project on October 15, 2016

Most fix-and-flip loans have a short maturity date, say one year at the outside. It’s assumed that in this time a prudent developer will be able to acquire a property, draw plans, pull permits, complete a rehab, and re-sell the home, paying off the loan at the close. The developer usually makes only the interest payment during this time (unless payments are deferred entirely), but once the loan term is up the entire balance and any back interest is due and payable all at once. The industry term for this is a “balloon payment.”

By the time the first year ran out, the Ebers project was far from complete, though it had begun to draw the ire of immediate neighbors and others in the Ocean Beach community. Complaints were raised about safe environmental practices not being followed when asbestos-laden materials were removed from the original house, and locals began questioning what looked like an entirely separate three-story house being built on the lot.

“I first learned about the place in late June, early July 2016,” explains Frank Gormlie, publisher of the Ocean Beach-centric OB Rag blog. “Some neighbors had put up a sign and a mannequin wearing a mask to complain about the way demolition was being handled on the smaller existing house.”

After meeting with the neighbors, Gormlie’s site took on a muckraking role, digging up dirt on the owners, the project, and the city. His activities, Gormlie explains over a mug at the Newbreak coffeehouse on Abbott Street where he’s greeted as a local by staff and patrons alike despite having moved from the neighborhood earlier in the decade, would result in increased scrutiny from the local planning board and protesters taking to the street. The topic was his site’s biggest draw for nearly a year.

“We eventually came up with a laundry list of issues — first was parking and whether it met the floor area ratio [a regulation that restricts improved square footage of a building to 70 percent of lot size, significantly lower than in other San Diego neighborhoods], it looked like it was over 30 feet high. But as we looked into it, it turns out there were all kinds of problems. Was this truly an addition, or was it two units?”

The project didn’t appear before the OB Planning Board, which usually offers input on proposed construction in the neighborhood, because it was represented to the city as a remodel of an existing single-family residence in permit applications. Such a classification would have allowed the project to dodge a coastal development permit typically required of beach-area development.

Thing is, Nelco never saw the property as a simple single-family remodel. In a failed attempt to sell the property in early 2016, notes on the expired listing state that the property “will be re-listed once 2nd unit is completed.”

“When you went to Curtis Nelson’s website, there he was very proudly talking about two units. But this was never supposed to be a multi-unit development,” Gormlie argues. “You’ve also got to consider the role of the city’s Development Services department, and the allowances they’ll give developers. Someone was asleep at the wheel on this project to progress to the point you could go in, pull a permit, and a new structure going up three stories before the community wound up feeling so violated they started demanding oversight on their own.

“It turns out there were two sets of plans submitted that didn’t match — and [Development Services] was asked how these could have gotten through and their response was ‘Oh, well they must have been reviewed by different people.’”

Construction inched along, at least until one final interruption. On August 6, 2016, one year and two days after the original purchase loans were funded, a fire broke out on the third story of the “addition.” Though damages were reported at a paltry $1000, fire investigators suspected arson was involved. No suspects were ever named.

OBecians, meanwhile, were ramping up their complaints. Dozens of residents gathered to picket the project in mid-October. Work had essentially ground to a halt following the fire. Days later the planning board, which Nelco had avoided asking for an opinion on the project, asked the city to issue a stop-work order following a raucous town hall meeting, essentially re-classifying the project so that it would be required to present plans to the community and apply for a coastal development permit.

“About 70 people showed up at the Ocean Beach Recreation Center where it was eventually voted to call on Mayor Faulconer’s office to issue a stop-work order,” Gormlie recalls. Of Nelco, “they were always invited [to events concerning the project] — they don’t show up, they don’t return calls, they don’t answer emails. They eventually issued a statement that we reprinted, it was total bullshit that didn’t address any of our issues.”

Following the protest, Nelco broke its silence and issued its only statement regarding project critics. The company insisted its goal was to be a good neighbor, and that unnamed modifications had been made to the plans to pacify locals, though it repeatedly emphasized that there was nothing wrong with the plans in the first place.

“The project conforms to all required municipal codes, city development regulations, and has obtained all required permits; it has been approved by City and County agencies . . . All components of this project have been stamped, approved and signed-off on by the City of San Diego to move forward with this project.”

Let’s get back to following the money. If the purchase loan for the property indeed had a one-year repayment period, that time would have passed two days prior to the fire, meaning the lien holders would be able to call their three notes due.

That didn’t happen, at least not immediately. In September 2016, Nelco obtained a new loan for $923,985 — this is the funding that would eventually come back to haunt Center Street Lending. The safe bet is that this paid off the previous $825,000 first mortgage, though it’s unclear whether a $110,000 second loan recorded at the time of Nelco’s purchase was paid off as well.

Canthus Property Group, the third and smallest lender among the original trio with a reported investment of only $14,000, appears to have been left out. In January 2017, Canthus filed a Notice of Default against Nelco, signaling their intent to foreclose on the property.

Anyone who holds a deed of trust against a property — California’s equivalent of the mortgage, trust deeds simplify and expedite the foreclosure process — can initiate foreclosure proceedings, but lien position matters. If the lender in first position, usually the one committing the most money to a borrower, wants to take legal action to force a property’s sale, they’re not beholden to anyone. Once a property goes up for public auction, any money raised goes to paying off the first loan, including late fees, back interest, and lawyers’ fees associated with filing the foreclosure. If there’s money left over, it goes next to the secondary lienholders, and after everyone who’s owed money associated with the property (which could also include contractors filing “mechanic’s liens” for unpaid work) is paid off, the remainder goes to the former owner.

For a lender in third position, then, foreclosing would be a bold move — if the Ebers Street parcel, with its fire-damaged shell of a building, didn’t fetch enough at auction to pay off Center Street and any other lenders with a position in front of the third, Canthus would be obligated to come up with more cash out-of-pocket to satisfy those loans before taking over ownership. Unless, that is, their position wasn’t as weak as it might have seemed.

Normally, lien position is determined in a straightforward manner — the first one to record a debt with the county is in first position, with later debts ranked second, third, and so forth. But if Center Street is going to commit nearly 70 times as much money to a project as tiny Canthus, they’re not going to want to be out-ranked when it comes time to collect. In these instances, any new major lender will require minor ones who aren’t being paid off to sign a subordination agreement — an acknowledgement that, even though their lien was filed first, it will still be in inferior position to the new first if it comes time to collect.

Did Center Street somehow miss the Canthus loan, neglecting to execute a subordination agreement and thus giving a group investing the equivalent of a used sedan’s value more control over the property than a bank with a nearly-million-dollar outlay? It’s possible.

In any case, we never get to see how this scenario plays out. In late March, a couple months after Canthus filed pre-foreclosure proceedings (despite California’s expedited process, foreclosure can still take five months or more), Nelco was able to raise even more capital — a $300,000 private money loan from an Albert Boyajian was recorded on March 28, followed quickly by another $60,000 loan from Alpha Omega Capital Group two days later. The Canthus foreclosure proceeding was quietly canceled, indicating a payoff finally took place.

By now, Nelco had managed to turn a $645,000 purchase price into somewhere between $1.3 and $1.4 million in outstanding loan debt, without having apparently committed any of the company’s own capital to the project. Not bad, considering construction had been halted on the project for nearly a year, the framework and strand board sheeting of the three-story “addition” having been left to rot in the unforgiving beach air.

A week before the latest $360,000 was poured into the project, Nelco’s Curtis Nelson had his contractor’s license suspended for failure to comply with the terms of an arbitration award related to another property. By June, Nelson’s license had been revoked by the state.

A few attempts were made to revise plans for the site, including the provision for a hallway to connect the two buildings and elimination of the second kitchen. By leaving the floorplan largely intact, a few quick modifications by a new owner once the city had signed off on the “remodel” work would have made it easy for a new owner to block off the hallway, finish the kitchen installation, and effectively have an illegal second unit up and running.

Again, things never progressed this far. Without an approved set of plans or a licensed contractor to oversee work, the buildings languished, falling into further disrepair as the spring and summer months drug on. By November 2017, trash piling up around the property and a homeless encampment that had sprung up in the unfinished garage forced the city to declare the site a public nuisance, and Nelco was issued an order to clean up and secure the property. Several weeks later, after a second fire broke out on the property (this one apparently set by squatters), the city took over the cleanup and boarded up the building.

Not that Nelco likely minded — two months earlier, Center Street had begun a second round of foreclosure proceedings, and after all the cash poured into the project with little to show in the way of progress, the developer was unlikely to raise a new round of capital.

The Ebers development turns out to be just one example of a series of Nelco investments that were simultaneously going belly-up at the time. Parcels across the county and as far away as Palm Springs, all of which had recorded liens well in excess of their reported sales prices at the time Nelco acquired them, were entering foreclosure one after another. They caught the eye of at least one out-of-town investor.

Tracy Smith is the chief executive of Downkicker Investments, a San Francisco-based outfit that focuses on fix-and-flip properties. We spoke in late 2017, shortly after Downkicker was able to obtain several other Nelco properties, including a cliffside estate on Barr Avenue near the UCSD Medical Center in Hillcrest. Sold for a reported $920,000 just weeks before Nelson lost his contractor’s license, Nelco was nonetheless able to obtain more than $2.1 million in loans against the property.

“I came in on behalf of a handful of secondary lien holders, negotiated directly with Nelco, and got him to buy out of the deal,” Smith said, explaining he’d been made aware of Nelco’s problems by a local broker with whom he shared investor clients. “I got him to accept a buyout at pennies on the dollar so he would just go away, he had already caused so many problems.”

Most of the secondary liens, Smith says, were structured in the form of a “shared-appreciation deed of trust — they were supposed to split the profits with Nelco from the proceeds of the flip.

“The negotiations with Nelco,” Smith continued, “were very, very difficult. There was six straight hours of old-school, boardroom-style negotiations around a table going back and forth. We were able to get it done for the benefit of the investors, but there’s certainly not a working relationship moving forward.”

While Downkicker eventually acquired title to four Nelco properties, more than a dozen more deals proved too complicated for Smith to untangle, including the Ebers board-up he referred to as “this monstrosity slapped in the middle of a quiet neighborhood.”

“I did conduct a meeting with 17 or 18 of his other investors, and there are a lot of angry people who don’t know where their money went on properties like Ebers. People in third position who thought they were in second, people with fourths who thought they were third, some of these deals even had fifth loans. There’s been a lot of money flying around and no one knows where it went.”

Smith concurs that some of the tactics Ocean Beach residents complained about with regard to permit dodging and ignoring local building codes were consistent with the developer’s general approach to business.

“There was just this constant shell game and shuffle, always trying to one-up or get over on somebody, and there was no transparency. On a Palm Springs property, for example, there was a kitchen and bath remodel permit pulled, then the whole house was gutted. Again, that’s trying to lie to the city about the size and scope of the work when you know full well you’re going to go in and do a complete remodel on a home.”

The Ebers Street saga finally closed its Nelco chapter on February 16, 2018 when, following a failed attempt to auction the property, ownership reverted to Center Street. The rest of Nelco’s once-booming portfolio seems to have met the same fate, as of mid-March the county assessor had no record of Nelco Properties holding an ownership stake in any San Diego real estate. A search of several known prior projects turned up a string of foreclosures in January and February, each time with the property ending up reverting to bank ownership. Center Street also ended up stuck with a house on Wabash Avenue in North Park, while Alpha Omega, the latecomer to the Ebers party, now has a North Park fixer of their own on the 3600 block of Polk Avenue.

Nelson himself seems committed to disappearing — the Nelco website has been taken down, as have all social media profiles, including the Instagram page where Nelson once bragged about the too-tall rooftop deck he envisioned for Ebers. Several attempts to contact Nelson dating back to mid-2017 have received no answer.

The Ebers property, meanwhile, has continued to languish in its abandoned state.

After the February foreclosure Boyajiian, a prominent Los Angeles area businessman and activist promoting Armenian causes, purchased the property from Center Street for a reported $925,000. By August, the city had once again posted abatement notices demanding the property be secured and the lot cleaned.

Boyajian, reached by phone in late September, says he has a total of $1.2 million tied up in the property, and is working with a new contractor to complete the construction — as a single-family home. He reports that new permits are currently being reviewed by the city. The project, once again, will not be presented to the community planning board.

“It’s like this boarded-up mini castle just standing on the corner of a busy street — stark and naked and ugly,” Gormlie laments. “It’s a monument to city incompetence, and to this day it’s a blight being forced on the community.”

Here's something you might be interested in.

A simple fix-and-flip can go horribly wrong

Will this part of Ebers Street ever be the same?

A simple fix-and-flip can go horribly wrong

Will this part of Ebers Street ever be the same?

A long-derided construction project at 2269 Ebers Street in Ocean Beach, spearheaded by Curtis Nelson of Nelco Properties, officially suffered its death blow this spring; after failing to attract a buyer at a foreclosure auction, ownership of the property reverted to Center Street Lending, an Irvine-based hard money lender that specializes in providing financing to “property flippers” seeking to buy low, complete a quick remodel, and resell properties at a significant profit.

Nelco’s ownership of the property – two short blocks off West Point Loma Boulevard and a block east of Sunset Cliffs Boulevard – was frequently controversial — at times the developer bragged on social media about his disregard for the coastal height limit, advertised his development as a two-unit property (it was permitted for only one residence), and drew fire from the community for allowing the property to fall into disrepair after illegal construction was halted by the city. But a dive into the financial history of the property offers an interesting look at how a simple fix-and-flip deal can go horribly wrong.

The original four-bedroom, two-bath home (right) and the expansion.

Nelco originally bought the four-bedroom, two-bath fixer for $645,000 in mid-2015. The home, built in 1927, sits about five blocks from Dog Beach and nine blocks from Newport Avenue, OB’s main drag. Residents here tend to be quieter and more entrenched in the OB lifestyle than the younger, more transient denizens of the neighborhood to the west locals refer to as the “war zone.”

Frank Gormlie’s OB Rag news blog drew attention to the illegal construction

San Diego’s multiple listing service indicates the home was paid for with cash, but that cash wasn’t necessarily Nelco’s. On the same day the sale was finalized, three separate loans were recorded against the property for a total of $949,000 — a full $304,000 more than the purchase price.

Experienced developers are often able to leverage other people’s money to fund their projects. That money, though, often comes at a high cost in the form of interest rates of 10 percent or more, compared to common conventional rates in the mid-4 percent range. Still, borrowing 147 percent of a home’s sale price is approaching exceptional, and we’re just getting started.

About 50 OB residents gathered to protest the project on October 15, 2016

Most fix-and-flip loans have a short maturity date, say one year at the outside. It’s assumed that in this time a prudent developer will be able to acquire a property, draw plans, pull permits, complete a rehab, and re-sell the home, paying off the loan at the close. The developer usually makes only the interest payment during this time (unless payments are deferred entirely), but once the loan term is up the entire balance and any back interest is due and payable all at once. The industry term for this is a “balloon payment.”

By the time the first year ran out, the Ebers project was far from complete, though it had begun to draw the ire of immediate neighbors and others in the Ocean Beach community. Complaints were raised about safe environmental practices not being followed when asbestos-laden materials were removed from the original house, and locals began questioning what looked like an entirely separate three-story house being built on the lot.

“I first learned about the place in late June, early July 2016,” explains Frank Gormlie, publisher of the Ocean Beach-centric OB Rag blog. “Some neighbors had put up a sign and a mannequin wearing a mask to complain about the way demolition was being handled on the smaller existing house.”

After meeting with the neighbors, Gormlie’s site took on a muckraking role, digging up dirt on the owners, the project, and the city. His activities, Gormlie explains over a mug at the Newbreak coffeehouse on Abbott Street where he’s greeted as a local by staff and patrons alike despite having moved from the neighborhood earlier in the decade, would result in increased scrutiny from the local planning board and protesters taking to the street. The topic was his site’s biggest draw for nearly a year.

“We eventually came up with a laundry list of issues — first was parking and whether it met the floor area ratio [a regulation that restricts improved square footage of a building to 70 percent of lot size, significantly lower than in other San Diego neighborhoods], it looked like it was over 30 feet high. But as we looked into it, it turns out there were all kinds of problems. Was this truly an addition, or was it two units?”

The project didn’t appear before the OB Planning Board, which usually offers input on proposed construction in the neighborhood, because it was represented to the city as a remodel of an existing single-family residence in permit applications. Such a classification would have allowed the project to dodge a coastal development permit typically required of beach-area development.

Thing is, Nelco never saw the property as a simple single-family remodel. In a failed attempt to sell the property in early 2016, notes on the expired listing state that the property “will be re-listed once 2nd unit is completed.”

“When you went to Curtis Nelson’s website, there he was very proudly talking about two units. But this was never supposed to be a multi-unit development,” Gormlie argues. “You’ve also got to consider the role of the city’s Development Services department, and the allowances they’ll give developers. Someone was asleep at the wheel on this project to progress to the point you could go in, pull a permit, and a new structure going up three stories before the community wound up feeling so violated they started demanding oversight on their own.

“It turns out there were two sets of plans submitted that didn’t match — and [Development Services] was asked how these could have gotten through and their response was ‘Oh, well they must have been reviewed by different people.’”

Construction inched along, at least until one final interruption. On August 6, 2016, one year and two days after the original purchase loans were funded, a fire broke out on the third story of the “addition.” Though damages were reported at a paltry $1000, fire investigators suspected arson was involved. No suspects were ever named.

OBecians, meanwhile, were ramping up their complaints. Dozens of residents gathered to picket the project in mid-October. Work had essentially ground to a halt following the fire. Days later the planning board, which Nelco had avoided asking for an opinion on the project, asked the city to issue a stop-work order following a raucous town hall meeting, essentially re-classifying the project so that it would be required to present plans to the community and apply for a coastal development permit.

“About 70 people showed up at the Ocean Beach Recreation Center where it was eventually voted to call on Mayor Faulconer’s office to issue a stop-work order,” Gormlie recalls. Of Nelco, “they were always invited [to events concerning the project] — they don’t show up, they don’t return calls, they don’t answer emails. They eventually issued a statement that we reprinted, it was total bullshit that didn’t address any of our issues.”

Following the protest, Nelco broke its silence and issued its only statement regarding project critics. The company insisted its goal was to be a good neighbor, and that unnamed modifications had been made to the plans to pacify locals, though it repeatedly emphasized that there was nothing wrong with the plans in the first place.

“The project conforms to all required municipal codes, city development regulations, and has obtained all required permits; it has been approved by City and County agencies . . . All components of this project have been stamped, approved and signed-off on by the City of San Diego to move forward with this project.”

Let’s get back to following the money. If the purchase loan for the property indeed had a one-year repayment period, that time would have passed two days prior to the fire, meaning the lien holders would be able to call their three notes due.

That didn’t happen, at least not immediately. In September 2016, Nelco obtained a new loan for $923,985 — this is the funding that would eventually come back to haunt Center Street Lending. The safe bet is that this paid off the previous $825,000 first mortgage, though it’s unclear whether a $110,000 second loan recorded at the time of Nelco’s purchase was paid off as well.

Canthus Property Group, the third and smallest lender among the original trio with a reported investment of only $14,000, appears to have been left out. In January 2017, Canthus filed a Notice of Default against Nelco, signaling their intent to foreclose on the property.

Anyone who holds a deed of trust against a property — California’s equivalent of the mortgage, trust deeds simplify and expedite the foreclosure process — can initiate foreclosure proceedings, but lien position matters. If the lender in first position, usually the one committing the most money to a borrower, wants to take legal action to force a property’s sale, they’re not beholden to anyone. Once a property goes up for public auction, any money raised goes to paying off the first loan, including late fees, back interest, and lawyers’ fees associated with filing the foreclosure. If there’s money left over, it goes next to the secondary lienholders, and after everyone who’s owed money associated with the property (which could also include contractors filing “mechanic’s liens” for unpaid work) is paid off, the remainder goes to the former owner.

For a lender in third position, then, foreclosing would be a bold move — if the Ebers Street parcel, with its fire-damaged shell of a building, didn’t fetch enough at auction to pay off Center Street and any other lenders with a position in front of the third, Canthus would be obligated to come up with more cash out-of-pocket to satisfy those loans before taking over ownership. Unless, that is, their position wasn’t as weak as it might have seemed.

Normally, lien position is determined in a straightforward manner — the first one to record a debt with the county is in first position, with later debts ranked second, third, and so forth. But if Center Street is going to commit nearly 70 times as much money to a project as tiny Canthus, they’re not going to want to be out-ranked when it comes time to collect. In these instances, any new major lender will require minor ones who aren’t being paid off to sign a subordination agreement — an acknowledgement that, even though their lien was filed first, it will still be in inferior position to the new first if it comes time to collect.

Did Center Street somehow miss the Canthus loan, neglecting to execute a subordination agreement and thus giving a group investing the equivalent of a used sedan’s value more control over the property than a bank with a nearly-million-dollar outlay? It’s possible.

In any case, we never get to see how this scenario plays out. In late March, a couple months after Canthus filed pre-foreclosure proceedings (despite California’s expedited process, foreclosure can still take five months or more), Nelco was able to raise even more capital — a $300,000 private money loan from an Albert Boyajian was recorded on March 28, followed quickly by another $60,000 loan from Alpha Omega Capital Group two days later. The Canthus foreclosure proceeding was quietly canceled, indicating a payoff finally took place.

By now, Nelco had managed to turn a $645,000 purchase price into somewhere between $1.3 and $1.4 million in outstanding loan debt, without having apparently committed any of the company’s own capital to the project. Not bad, considering construction had been halted on the project for nearly a year, the framework and strand board sheeting of the three-story “addition” having been left to rot in the unforgiving beach air.

A week before the latest $360,000 was poured into the project, Nelco’s Curtis Nelson had his contractor’s license suspended for failure to comply with the terms of an arbitration award related to another property. By June, Nelson’s license had been revoked by the state.

A few attempts were made to revise plans for the site, including the provision for a hallway to connect the two buildings and elimination of the second kitchen. By leaving the floorplan largely intact, a few quick modifications by a new owner once the city had signed off on the “remodel” work would have made it easy for a new owner to block off the hallway, finish the kitchen installation, and effectively have an illegal second unit up and running.

Again, things never progressed this far. Without an approved set of plans or a licensed contractor to oversee work, the buildings languished, falling into further disrepair as the spring and summer months drug on. By November 2017, trash piling up around the property and a homeless encampment that had sprung up in the unfinished garage forced the city to declare the site a public nuisance, and Nelco was issued an order to clean up and secure the property. Several weeks later, after a second fire broke out on the property (this one apparently set by squatters), the city took over the cleanup and boarded up the building.

Not that Nelco likely minded — two months earlier, Center Street had begun a second round of foreclosure proceedings, and after all the cash poured into the project with little to show in the way of progress, the developer was unlikely to raise a new round of capital.

The Ebers development turns out to be just one example of a series of Nelco investments that were simultaneously going belly-up at the time. Parcels across the county and as far away as Palm Springs, all of which had recorded liens well in excess of their reported sales prices at the time Nelco acquired them, were entering foreclosure one after another. They caught the eye of at least one out-of-town investor.

Tracy Smith is the chief executive of Downkicker Investments, a San Francisco-based outfit that focuses on fix-and-flip properties. We spoke in late 2017, shortly after Downkicker was able to obtain several other Nelco properties, including a cliffside estate on Barr Avenue near the UCSD Medical Center in Hillcrest. Sold for a reported $920,000 just weeks before Nelson lost his contractor’s license, Nelco was nonetheless able to obtain more than $2.1 million in loans against the property.

“I came in on behalf of a handful of secondary lien holders, negotiated directly with Nelco, and got him to buy out of the deal,” Smith said, explaining he’d been made aware of Nelco’s problems by a local broker with whom he shared investor clients. “I got him to accept a buyout at pennies on the dollar so he would just go away, he had already caused so many problems.”

Most of the secondary liens, Smith says, were structured in the form of a “shared-appreciation deed of trust — they were supposed to split the profits with Nelco from the proceeds of the flip.

“The negotiations with Nelco,” Smith continued, “were very, very difficult. There was six straight hours of old-school, boardroom-style negotiations around a table going back and forth. We were able to get it done for the benefit of the investors, but there’s certainly not a working relationship moving forward.”

While Downkicker eventually acquired title to four Nelco properties, more than a dozen more deals proved too complicated for Smith to untangle, including the Ebers board-up he referred to as “this monstrosity slapped in the middle of a quiet neighborhood.”

“I did conduct a meeting with 17 or 18 of his other investors, and there are a lot of angry people who don’t know where their money went on properties like Ebers. People in third position who thought they were in second, people with fourths who thought they were third, some of these deals even had fifth loans. There’s been a lot of money flying around and no one knows where it went.”

Smith concurs that some of the tactics Ocean Beach residents complained about with regard to permit dodging and ignoring local building codes were consistent with the developer’s general approach to business.

“There was just this constant shell game and shuffle, always trying to one-up or get over on somebody, and there was no transparency. On a Palm Springs property, for example, there was a kitchen and bath remodel permit pulled, then the whole house was gutted. Again, that’s trying to lie to the city about the size and scope of the work when you know full well you’re going to go in and do a complete remodel on a home.”

The Ebers Street saga finally closed its Nelco chapter on February 16, 2018 when, following a failed attempt to auction the property, ownership reverted to Center Street. The rest of Nelco’s once-booming portfolio seems to have met the same fate, as of mid-March the county assessor had no record of Nelco Properties holding an ownership stake in any San Diego real estate. A search of several known prior projects turned up a string of foreclosures in January and February, each time with the property ending up reverting to bank ownership. Center Street also ended up stuck with a house on Wabash Avenue in North Park, while Alpha Omega, the latecomer to the Ebers party, now has a North Park fixer of their own on the 3600 block of Polk Avenue.

Nelson himself seems committed to disappearing — the Nelco website has been taken down, as have all social media profiles, including the Instagram page where Nelson once bragged about the too-tall rooftop deck he envisioned for Ebers. Several attempts to contact Nelson dating back to mid-2017 have received no answer.

The Ebers property, meanwhile, has continued to languish in its abandoned state.

After the February foreclosure Boyajiian, a prominent Los Angeles area businessman and activist promoting Armenian causes, purchased the property from Center Street for a reported $925,000. By August, the city had once again posted abatement notices demanding the property be secured and the lot cleaned.

Boyajian, reached by phone in late September, says he has a total of $1.2 million tied up in the property, and is working with a new contractor to complete the construction — as a single-family home. He reports that new permits are currently being reviewed by the city. The project, once again, will not be presented to the community planning board.

“It’s like this boarded-up mini castle just standing on the corner of a busy street — stark and naked and ugly,” Gormlie laments. “It’s a monument to city incompetence, and to this day it’s a blight being forced on the community.”