{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Escondido maintenance man loses home to foreclosure defrauders

The unscrupulous Zepeda brothers

At least 550 Southern California homeowners

have been victimized by the Zepeda brothers.

Benito Cristobal is surveying the house he lost last year to a foreclosure defrauder, and he is emotional as he recalls the $30,000 worth of improvements he made to the home. The 51-year-old Mexican-American maintenance man, his son Efrem, a high school senior, silent by his side, steps slowly around what he once possessed, his gestures grand, his voice regretful. He says he got rid of the garden and laid concrete walkways. He covered the ground under the three lemon trees with redwood chips. He bought a new water heater, new windows, gutters. He built a patio with a roof, though he had to remove the roof and saw off the struts once the city discovered the unpermitted structure. He built a low cement-block wall, with a black wrought-iron fence atop, to surround the four 30-foot palms. For seven golden years, this three-bedroom, two-bath, two-car-garage abode was his and his family’s — at least on paper.

Benito Cristobal and his son Efrem in front of the house they lost to a foreclosure defrauder.

The home at 700 East Washington Avenue in Escondido cost Cristobal $390,000 in 2004. After he lost the 1144-square-foot home a year ago, it was sold for $145,000 — a 63 percent drop. Now, in 2012, it is for sale again at $237,500. A banner above the garage reads, “Buy this home for 3% down!” (Weren’t these teaser loans precisely what drove borrowers like Cristobal into the mortgage meltdown?) Today, the beige house with brown trim sits unloved and empty on an indifferent corner in central Escondido.

After living in the home for six years, in early 2010, Cristobal was laid off from one of his maintenance jobs in Vista. Soon, he fell behind on payments to Bank of the West. He paid the mortgage with his savings until that fund was exhausted. He called the bank, repeatedly trying to set up a loan modification. The bank never called back. His debt mounted.

In July 2010, a friend told him there was a Spanish-speaking business, Sunset Beach Management, in Downey, California, that would modify his loan. He and his friend drove to Downey and heard the pitch, he remembers, from a host of operatives: Alex Canjurra and Yesenia Mendoza; a money-handler, Eddie Teran; and the office boss, Lucy Delgado.

How much to save the Escondido house from foreclosure?

The processing fee was $2995. On top of that, Cristobal needed to pay the monthly mortgage, $1534, to Sunset Beach. Cristobal went home, thought it over, then got cashier’s checks — he shakes his head now, showing me his receipts — and hand-delivered them to the Downey office the following week. Lucy Delgado told him, “Not to worry. We take care of everything.” One other catch: before leaving, she asked him to sign a quitclaim deed. This would clinch the deal: his Escondido home would be signed over to the David Zepeda Trust — the only way to avoid foreclosure.

Who was David Zepeda? The head of the company.

Cristobal complied.

Beginning in July 2010 and for the next five months, Cristobal made payments first to Sunset Beach, then, after a company name change in September, to “FWHLA,” Financial Wellness for Homeowners of Los Angeles. In early 2011, parking his truck in his driveway, he saw a notice tacked on the garage door. His house was up for auction. He called the money-handler, Eddie Teran. “Fax me that paper and don’t worry,” Teran told him. “Everything’s going to be all right.”

The day before Cristobal drove to Downey to deliver the next check, someone from Financial Wellness called and said that the company had changed hands. It was part of Zap Group Legal, in Woodland Hills — no longer David Zepeda’s but now run by Eddie Teran. Cristobal froze in his tracks. He had never received any loan-modification papers — from his new or his old lienholder. He threw his keys on the counter and slumped into a chair. He was done getting cashier’s checks and rushing them to Teran.

Last summer, the property went into foreclosure and Cristobal was evicted. Broke, his only option was to declare bankruptcy. Benito and Efrem left the Washington Avenue house and moved in with Benito’s daughter, about three blocks away.

Though he has restarted his life with a backyard nursery — a sign out front reads Muchas Plantas Diferentes — he is still angry. He filed suit in Vista small claims court against Sunset Beach and won a judgment, $7500, by default. Shaking his head again, he says that is money he will never see. He holds a scintilla of hope that someday after both Zepeda brothers are convicted he might get a small portion of the thousands of dollars he’s lost.

Last February, John Zepeda pled guilty to forgery, filing false deeds, and rent skimming. (David Zepeda’s case has yet to go to trial.) At John’s sentencing in superior court, Cristobal spoke, the only victim to come forward. “Everybody is scared,” he said. “These two [Zepeda brothers] and the others” — referring to office managers and bagmen — “are like the Mafia. I was told I would get a modification for my loan. It never happened. Please, Judge, let justice be done.”

Outside the courtroom, recounting his ordeal to reporters, he halted in midsentence. Under the light of a TV camera, he teared up. “What they promise is not true,” he said, his voice cracking, a touch of shame leaking through. “It is so hard to trust people now. Please don’t trust anyone who says they will help you.”

Unconscionable, Evil

Like an octopus, the massive loan-modification scheme, beginning in January 2006 and created by the Zepeda brothers, reached its tentacles into the lives of hundreds of Southern Californians. Starting in San Bernardino and moving into adjacent counties, the fraud netted millions of dollars in mortgage payments and fees as the crooks bamboozled desperate homeowners.

The Zepeda brothers ran one of three prominent rings that operated in Southern California over the past six years. The rings were composed of families or employees of those families who set up operations in dozens of Hispanic neighborhoods, including Orange, Los Angeles, and San Diego counties, Ventura, Riverside, and Kern counties, as well as urban areas of Nevada and Arizona. (One term used for schemes that involve ethnicity is “affinity fraud.”) Members of the rings would teach — and game — each other. A group of employees would organize its own cadre and bring in new people to do the dirty work.

In 2006, home buying had reached a tipping point. The price of homes, after soaring for several years, peaked and began to fall. Homeowners, many of whom were given teaser loans based on faked or no documentation, faced sudden balloon payments and found themselves unable to pay.

As mortgage holders fell behind in their payments, David Zepeda set up the first ring, opening a mortgage refinancing office in San Bernardino. According to court documents, Luis Macias, a notary, was selling prepaid cell phones at a storefront down the street. Yunuen Medina, who is described as “a Hispanic female, 5ʹ tall, 110 pounds, with black hair,” came into Macias’s business to buy a phone. A matchmaker of sorts, Medina had already met Zepeda, and she introduced the two men.

At the time, Macias was facing foreclosure on his home. Zepeda, who with his brother John had already defrauded a few underwater homeowners, told Macias that if he quitclaimed his house to Zepeda, the bank would have trouble seizing it. Macias signed the deed, conveying the property to the David Zepeda Trust. Then Zepeda lowered the boom. Macias would have to move out of the house so that Zepeda could rent it. Macias realized he’d been snookered.

Macias got an idea. Call it a reverse golden rule. Why not do unto others what the defrauder Zepeda had done unto him?

Such was the way the scheme gained momentum, said Vance Welch, a deputy district attorney with the real estate fraud unit of San Bernardino County. Welch portrayed the David Zepeda–Luis Macias link as one of “mentor and disciple.” A victim would set up his own dummy loan-modification business in a part of town that Zepeda had not yet colonized. Welch compared the Zepeda contagion to a Ponzi. A victim says, “I’ll try and recoup my losses from the people I’m going to screw in the future.”

Under Macias’s leadership, a company called Home Recovery Trust was born. The Macias-Medina ring set up its business office in Rialto, one town west of the city of San Bernardino. The pair advertised their services in Hispanic communities, principally on TV and radio. Welch said that in Medina’s Spanish-language commercials, she “would tout herself as a successful woman.” At 23, she was young and attractive, a self-made immigrant. Welch noted that she would claim, “‘I used to be beaten by my husband, but I went out and took my own initiative and now I’m working for this great company, Home Recovery Trust, who can save your home.’ Then she outlined the program.”

Home Recovery Trust grew, Welch said, doing especially well in churches, where “Yunuen was very active” and where she’d offer seminars on alternatives to foreclosure. “A lot of our victims,” Welch said, “came from churches.” Soon, desperate homeowners were coming into the Rialto office and signing documents left and right.

The ring’s quitclaim deeds, falsely notarized by a woman named Reina Rogers, were transferred to the Michael Martinez Trust, another dummy entity. In addition, Home Recovery Trust required its clients to pay up-front fees (between $2500 and $3500) and make monthly rent or mortgage payments to the trust as well as sign powers of attorney.

Bank records showed that Macias and Medina took in more than $5 million. Maurice Landrum, senior investigator with the San Bernardino County district attorney’s office, said that Macias “personally withdrew” a little over $1 million “based on bank slips signed by him.”

Macias lived “like a rock star,” Welch said. “He rented a big portion of the Queen Mary to renew his vows with his wife,” bringing in guests via hired limo. He paid “$17,000 to rent a yacht. There were expensive hotels, clothes, the whole bit. If you had a chance then to see the victims — a blind lady, an elderly couple with a 35-year-old daughter in a wheelchair — and Macias was sitting across the table from them, saying, ‘We will save your house. Just keep sending us the money.’ It’s unconscionable. It’s just evil.”

In 2010, the Macias-Medina ring was busted. Ten people were arrested and all of them pled guilty.

Luis Macias was arrested April 20, 2010, in the hallway of the San Bernardino County superior courthouse, where he was facing, according to a district attorney’s press release, “felony charges in another real-estate-related fraud case.” For the felony charges with Home Recovery Trust he got five years and eight months in state prison. The trust was valued at $350,000, a paltry slice of the $5 million it had taken in. Restitution payments for the more than 450 victims have not yet been awarded.

Yunuen Medina served 180 days in county jail. She was then deported.

Big Day

The original ring involved David Zepeda and his brother John. About the time investigators were closing in on Macias and Medina, they were learning where the pair had gotten their training: from the mastermind David Zepeda.

The story of David Zepeda begins with his end — a day in August 2010 when Maurice Landrum had a crazy bit of luck. That day he happened to be checking crime reports. He found one that a David Zepeda had filed. Landrum knew the name. Sheriff’s deputies had been investigating Zepeda for real estate fraud, although they didn’t have his current address. Someone, Zepeda complained in the report, had thrown a rock through the window of his Bentley.

“Crooks always do something stupid to lead you to them.” Sheriff’s deputies found David Zepeda after he filed

a report that his Bentley had been vandalized.

Zepeda had bought a white Bentley sedan with white leather upholstery from Las Vegas Motor Cars and paid with a cashier’s check for $78,602. He’d parked the car in the driveway of his North Ofelia Drive home, located on a cul-de-sac in a new enclave in San Bernardino, close to the I-15 and I-215 merge. Eyeing window glass strewn through the Bentley’s lush interior, he called to report the crime so that his insurance would pay for the repair.

Though he was surprised, Landrum shouldn’t have been. “Crooks always do something stupid to lead you to them,” he said. He began surveillance and notified James Motz, an investigator for the real estate fraud division in the district attorney’s office in San Diego. Authorities here had gotten many complaints, as had the California Department of Real Estate, about loan-modification companies working in Vista, Fallbrook, Chula Vista, and elsewhere. The San Diego district attorney’s office had put Motz on the case.

On September 2, 2010, Landrum said that he, sheriff’s deputies, and Motz “hit the house.” Inside, they found John Zepeda. John, they didn’t know about. John said that David was in intensive care at Kaiser hospital in nearby Fontana. Leaving others to search the house, Landrum drove to the hospital and found David. Weighing nearly 300 pounds, in bed, and on a breathing tube, he had suffered a stroke one week earlier. San Diego court documents quote John Zepeda as saying at the time that doctors believed David “will neither walk nor talk again.”

Landrum arrived back at the house in time to hear John admitting to the real estate scheme with his brother. He began pulling out the drawers of his desk, then opened the safe in the master bedroom. He took investigators to a second bedroom where piles of forged documents lay. There they were — the fake notary stamps with the names of San Diego notaries Bill Washington, Karla and Joel Magana, Mark Desahagun, among many others. “It was unbelievable,” Landrum recalled. “If we hadn’t recorded it, nobody would have believed us.”

In the Zepeda brothers’ garage Landrum found a truck that contained a “treasure trove” of incriminating material. “The San Diego false [quitclaim] deeds, the San Bernardino false deeds, P.O. boxes in San Ysidro where the stuff was going — it was beautiful.”

In the meantime, investigator Motz got arrest warrants in San Diego for the brothers. They would be tried here first: the evidence of their crimes in San Diego County was strongest. Motz arrested John and David, although David had to remain in the hospital. Motz drove John to the San Diego jail.

Investigators found 8320 coins at Zepeda’s house, along with hundreds of thousands of dollars’ worth of cash, gold, jewelry, guns, and cashier’s checks.

From the house, the garage, and the truck, investigators collected $335,000 in cashier’s checks. In a closet they found a Thompson submachine gun, a Mossberg shotgun, and a Ruger Mini-14 with a folding stock. From the safe they catalogued a gold-colored Geneva watch, a gold-colored Rolex, and several diamond bracelets, necklaces, and rings. There was $31,502 in cash; 13 boxes of silver coins with 640 coins per box, totaling 8320; and several hundred boxes of gold troy ounces. In the end, the San Diego district attorney’s office collected 120 banker boxes of evidence, including records of quitclaim deeds from 400 homeowners; rent payments from many of those homeowners, made out to the David Zepeda Trust; and more than 400 forgeries of notary signatures on quitclaim deeds, all of which were filed with the San Diego County Recorder.

In a news conference at the time, district attorney Bonnie Dumanis charged the brothers with 106 felony counts as well as 215 “overt acts” of foreclosure fraud. The felonies included multiple counts each of conspiracy, forgery, using the personal identifying information of another, rent skimming, filing false instruments, and grand theft.

David Zepeda is now in custody in San Diego. Welch said that after the Zepeda brothers’ trials have finished in San Diego, he will file his case against them in San Bernardino. He is ready to go to trial with 74 counts against the brothers.

How the Zepedas Worked the Scheme

In early 2006, after David Zepeda formed Sunset Trust, changed later to Sunset Beach Management, he would drive around San Bernardino looking for distressed properties — anything to suggest a foreclosure in progress and an empty home. An overgrown yard, a cracked window, newspapers piling up in the driveway. Zepeda would place a For Rent sign, with his San Bernardino phone number, in the front yard.

He also researched foreclosure proceedings and contacted the underwater homeowner. He might, as a person commented on the Fallbrook Village News website, knock on the front door, “flash a badge [and say he was] employed . . . by a city’s code enforcement division.” Then he would tell the distressed owner that he knew of a company, Sunset Beach Management, that could save his or her property.

In his criminal complaint, Motz described the scheme. Once the Zepeda brothers identified a foreclosure, they had the homeowner sign a quitclaim deed or John would forge one, and John would forge the name of a local notary onto the deed: the names could not be fabricated because the county recorder’s office would check both names when the deed was filed.

Next, Motz wrote, David Zepeda “rents out the property, in most cases for over a thousand dollars per month.” To “forestall the foreclosure process,” he would transfer the property from one trust to another. He would also buy time — to collect more rent — by filing a bankruptcy petition for the homeowner. “Money is diverted away from the lenders and owners and into Zepeda’s accounts,” Motz wrote. “Zepeda then uses the rent money to support a lavish lifestyle, including the purchase of multiple luxury, high-end automobiles and travel.”

The Torres Family Joins the Circus

Maurice Landrum described yet another ring — a third — composed of Carlos Torres, his sister Patricia, and their father Manuel. Carlos had “learned the Zepedas’ system and branched out” on his own in San Diego. Oscar Macias (unrelated to Luis Macias) was an associate of the Torreses and the Zepedas.

In San Diego, the Torres ring filed about a dozen quitclaim deeds, transferring property to the Carlos Torres Trust. In San Bernardino, two of the people Carlos defrauded were law enforcement officers, who, according to the district attorney’s press release, “were unaware that their names had been forged on quitclaim deeds, or their properties had been rented out.”

After multiple investigations in 2009 and 2010, the case went to the San Bernardino grand jury. Arrest warrants were issued for, among others, Carlos, Patricia, and Manuel Torres and their associate Oscar Macias.

In spring 2010, Landrum arrested Carlos Torres at the federal prison at Lompoc. Torres was serving a two-year sentence, having pled guilty to another charge — conspiracy to transport illegal aliens in California. Vance Welch, San Bernardino deputy district attorney, said that “Carlos is into a lot weirder stuff than we just had him for.”

In San Bernardino superior court, Carlos Torres pled guilty on June 10, 2010, to forgery and conspiracy to commit felony real estate fraud. He received two years in a state prison. The father, Manuel, pled guilty to the same charges, got 120 days in county jail, and received three years’ felony probation. Oscar Macias, a stout, shaved-head bagman, also pled guilty and received time served.

In October of 2010, prosecutors in San Diego indicted David Zepeda, Carlos Torres, and Patricia Torres on charges of forgery, conspiracy, and filing false documents.

It’s not a stretch to say that San Bernardino deputy district attorney Welch sounds livid, thinking back on five years of the Southland’s big uptick in foreclosure fraud. “Sometimes I feel like I’m standing on a beach holding back a wave,” he says. San Diego has been the “only county” to cooperate in investigating and prosecuting these multijurisdictional crimes. Neither his office nor San Diego’s, he says, has the resources to nail every fraudulent loan modifier. “We will pick and choose where [prosecutions] will make the greatest impact and that will send the message that you don’t do it here.”

Welch says he wishes that more county and state officials would get involved. But, he notes, the “egos are just too big” in Los Angeles, Riverside, and Orange counties for their fraud divisions to collaborate with him. What’s more, recent and current attorneys general — Jerry Brown and Kamala Harris — promised to prosecute these illegal rings but so far they have not. “Everything we referred to the [state] attorney general’s office got sent back.”

The State’s Oversight

The California Department of Real Estate issues a “desist and refrain” order when an investigation reveals that people who do not have a real estate license are acting as real estate brokers. This includes negotiating the sale of real property, soliciting for prospective tenants, and performing services for borrowers in connection with loans secured by liens on real property. Operating without a license is a violation of the California Business and Professions Code. David Zepeda and 34 other people, trusts, and businesses were ordered on January 26, 2012, to desist and refrain from performing acts for which a real estate broker license is required.

The department of real estate investigation found that at least 550 Southern California homeowners have been victimized by the Zepeda brothers. One variation of the loan-modification scheme was called the “caretaker plan.” The homeowner quitclaims their house, bequeathing it to a trust, and pays rent and fees to the trust. They’re told that once the trust collects several deeds, its trustees will pool the “homeowner monies” in order to purchase the notes from the homeowners’ lenders. Eventually, the trust, so the plan goes, sells the property back to the homeowner at a lower cost. The problem is, such packaging, which sounds good to a distressed debtor, is all shine. There is no pool of money to purchase the homes. The money has been spent. Plus there is no modified loan that can be negotiated between lender and homeowner. No bank is involved. The caretaker plan is styled as a way to buy time and to keep the property from foreclosure. Just the opposite occurs. Most homeowners lose their properties to foreclosure and are evicted.

Tom Pool, spokesperson for the department of real estate, says there are several reasons why foreclosure fraud has mushroomed in the past five years. First, lenders have not had the resources to deal with the volume of defaults, late payments, and requests for loan modifications. Second, federal and state laws, some enacted as the crisis developed, require lenders to make mortgage adjustments, though much anecdotal evidence suggests that adjustments are not being made. (SB 1137, a mortgage relief bill passed in 2008, requires that lenders contact delinquent homeowners and negotiate a loan modification 30 days before sending them a notice of default.) Then there are delays the law requires: notice of default, a 90-day waiting period before the foreclosure process begins, and more. Add to that a bankruptcy filing on the part of a homeowner or trust, again to buy time, and one founders in the swamp of delay. With such a bog of rules, the average time it takes a foreclosure to be processed is 260 days.

One Little Fish, One Big Piranha

One of the many curiosities about John Zepeda, who reached a plea agreement with San Diego prosecutors in December of 2011, is that his attorney, deputy public defender Kathleen Coyne, insisted that he was only peripherally involved. John was David’s notary forger — just an employee. In his San Bernardino home office, he made the fake notary stamps, then stamped them on the fake quitclaim deeds and forged the notary’s signature. He was a little fish compared to David, the piranha, so Coyne said. But the judge didn’t buy her defense. After John pled guilty to 13 felony counts — using personal information of another, forging checks and money orders, filing false instruments, and rent skimming — the judge sentenced him to 12 years in state prison, minus the 534 days that he'd already been locked up.

John Zepeda in court

The “restitution floor amount” in the Zepeda brothers’ case has been put at $6 million in San Diego. The district attorney’s office has put the number of local victims at 40, with 26 properties involved. And yet the worth of the Zepeda brothers’ ring, which overlaps with the Torres family ring, is estimated at only $200,000 or $300,000, similar to the Macias-Medina ring. As part of John Zepeda’s sentence, the judge ruled that the fine against him be reduced from $10,000 to $200. This ruling makes more money — but not much — available for victims. Whether or not those victims, which includes the lending institutions, will get any money remains to be seen. The court assigns a forensic accountant to cull through those 120 boxes and unravel the web of bank accounts. The restitution hearings won’t occur until after David Zepeda’s trial.

San Diego Crooks Finally Sentenced

For months of hearings, Patricia Torres came to court wearing an ankle lock, its green light flashing. In April, she pled guilty, her agreement including a maximum of six years in state prison. She will be sentenced July 13.

The same month, her brother Carlos pled guilty to conspiracy and was sentenced to three years and four months. This term is to be served consecutively with the time remaining on his federal sentence for transporting illegal aliens into the country.

In part because of David Zepeda’s stroke, his fragile health, and the complexity of the case, his defense attorneys have asked the court several times to postpone their client’s trial. At hearings in which Zepeda has appeared, the wait to begin is extra long. He must be transported from a local facility where ill prisoners are kept. The bailiff brings him in in a wheelchair. Zepeda is slumped and motionless. His gray beard and graying sidewalls, his eerie stillness, give him a near-hospice look. The bailiff announces to the judge that Zepeda can’t hear well: attorneys must stand near him and state charges and motions in a mild shout. His trial is currently scheduled to begin on July 23.

Here's something you might be interested in.

Escondido maintenance man loses home to foreclosure defrauders

The unscrupulous Zepeda brothers

Escondido maintenance man loses home to foreclosure defrauders

The unscrupulous Zepeda brothers

At least 550 Southern California homeowners

have been victimized by the Zepeda brothers.

Benito Cristobal is surveying the house he lost last year to a foreclosure defrauder, and he is emotional as he recalls the $30,000 worth of improvements he made to the home. The 51-year-old Mexican-American maintenance man, his son Efrem, a high school senior, silent by his side, steps slowly around what he once possessed, his gestures grand, his voice regretful. He says he got rid of the garden and laid concrete walkways. He covered the ground under the three lemon trees with redwood chips. He bought a new water heater, new windows, gutters. He built a patio with a roof, though he had to remove the roof and saw off the struts once the city discovered the unpermitted structure. He built a low cement-block wall, with a black wrought-iron fence atop, to surround the four 30-foot palms. For seven golden years, this three-bedroom, two-bath, two-car-garage abode was his and his family’s — at least on paper.

Benito Cristobal and his son Efrem in front of the house they lost to a foreclosure defrauder.

The home at 700 East Washington Avenue in Escondido cost Cristobal $390,000 in 2004. After he lost the 1144-square-foot home a year ago, it was sold for $145,000 — a 63 percent drop. Now, in 2012, it is for sale again at $237,500. A banner above the garage reads, “Buy this home for 3% down!” (Weren’t these teaser loans precisely what drove borrowers like Cristobal into the mortgage meltdown?) Today, the beige house with brown trim sits unloved and empty on an indifferent corner in central Escondido.

After living in the home for six years, in early 2010, Cristobal was laid off from one of his maintenance jobs in Vista. Soon, he fell behind on payments to Bank of the West. He paid the mortgage with his savings until that fund was exhausted. He called the bank, repeatedly trying to set up a loan modification. The bank never called back. His debt mounted.

In July 2010, a friend told him there was a Spanish-speaking business, Sunset Beach Management, in Downey, California, that would modify his loan. He and his friend drove to Downey and heard the pitch, he remembers, from a host of operatives: Alex Canjurra and Yesenia Mendoza; a money-handler, Eddie Teran; and the office boss, Lucy Delgado.

How much to save the Escondido house from foreclosure?

The processing fee was $2995. On top of that, Cristobal needed to pay the monthly mortgage, $1534, to Sunset Beach. Cristobal went home, thought it over, then got cashier’s checks — he shakes his head now, showing me his receipts — and hand-delivered them to the Downey office the following week. Lucy Delgado told him, “Not to worry. We take care of everything.” One other catch: before leaving, she asked him to sign a quitclaim deed. This would clinch the deal: his Escondido home would be signed over to the David Zepeda Trust — the only way to avoid foreclosure.

Who was David Zepeda? The head of the company.

Cristobal complied.

Beginning in July 2010 and for the next five months, Cristobal made payments first to Sunset Beach, then, after a company name change in September, to “FWHLA,” Financial Wellness for Homeowners of Los Angeles. In early 2011, parking his truck in his driveway, he saw a notice tacked on the garage door. His house was up for auction. He called the money-handler, Eddie Teran. “Fax me that paper and don’t worry,” Teran told him. “Everything’s going to be all right.”

The day before Cristobal drove to Downey to deliver the next check, someone from Financial Wellness called and said that the company had changed hands. It was part of Zap Group Legal, in Woodland Hills — no longer David Zepeda’s but now run by Eddie Teran. Cristobal froze in his tracks. He had never received any loan-modification papers — from his new or his old lienholder. He threw his keys on the counter and slumped into a chair. He was done getting cashier’s checks and rushing them to Teran.

Last summer, the property went into foreclosure and Cristobal was evicted. Broke, his only option was to declare bankruptcy. Benito and Efrem left the Washington Avenue house and moved in with Benito’s daughter, about three blocks away.

Though he has restarted his life with a backyard nursery — a sign out front reads Muchas Plantas Diferentes — he is still angry. He filed suit in Vista small claims court against Sunset Beach and won a judgment, $7500, by default. Shaking his head again, he says that is money he will never see. He holds a scintilla of hope that someday after both Zepeda brothers are convicted he might get a small portion of the thousands of dollars he’s lost.

Last February, John Zepeda pled guilty to forgery, filing false deeds, and rent skimming. (David Zepeda’s case has yet to go to trial.) At John’s sentencing in superior court, Cristobal spoke, the only victim to come forward. “Everybody is scared,” he said. “These two [Zepeda brothers] and the others” — referring to office managers and bagmen — “are like the Mafia. I was told I would get a modification for my loan. It never happened. Please, Judge, let justice be done.”

Outside the courtroom, recounting his ordeal to reporters, he halted in midsentence. Under the light of a TV camera, he teared up. “What they promise is not true,” he said, his voice cracking, a touch of shame leaking through. “It is so hard to trust people now. Please don’t trust anyone who says they will help you.”

Unconscionable, Evil

Like an octopus, the massive loan-modification scheme, beginning in January 2006 and created by the Zepeda brothers, reached its tentacles into the lives of hundreds of Southern Californians. Starting in San Bernardino and moving into adjacent counties, the fraud netted millions of dollars in mortgage payments and fees as the crooks bamboozled desperate homeowners.

The Zepeda brothers ran one of three prominent rings that operated in Southern California over the past six years. The rings were composed of families or employees of those families who set up operations in dozens of Hispanic neighborhoods, including Orange, Los Angeles, and San Diego counties, Ventura, Riverside, and Kern counties, as well as urban areas of Nevada and Arizona. (One term used for schemes that involve ethnicity is “affinity fraud.”) Members of the rings would teach — and game — each other. A group of employees would organize its own cadre and bring in new people to do the dirty work.

In 2006, home buying had reached a tipping point. The price of homes, after soaring for several years, peaked and began to fall. Homeowners, many of whom were given teaser loans based on faked or no documentation, faced sudden balloon payments and found themselves unable to pay.

As mortgage holders fell behind in their payments, David Zepeda set up the first ring, opening a mortgage refinancing office in San Bernardino. According to court documents, Luis Macias, a notary, was selling prepaid cell phones at a storefront down the street. Yunuen Medina, who is described as “a Hispanic female, 5ʹ tall, 110 pounds, with black hair,” came into Macias’s business to buy a phone. A matchmaker of sorts, Medina had already met Zepeda, and she introduced the two men.

At the time, Macias was facing foreclosure on his home. Zepeda, who with his brother John had already defrauded a few underwater homeowners, told Macias that if he quitclaimed his house to Zepeda, the bank would have trouble seizing it. Macias signed the deed, conveying the property to the David Zepeda Trust. Then Zepeda lowered the boom. Macias would have to move out of the house so that Zepeda could rent it. Macias realized he’d been snookered.

Macias got an idea. Call it a reverse golden rule. Why not do unto others what the defrauder Zepeda had done unto him?

Such was the way the scheme gained momentum, said Vance Welch, a deputy district attorney with the real estate fraud unit of San Bernardino County. Welch portrayed the David Zepeda–Luis Macias link as one of “mentor and disciple.” A victim would set up his own dummy loan-modification business in a part of town that Zepeda had not yet colonized. Welch compared the Zepeda contagion to a Ponzi. A victim says, “I’ll try and recoup my losses from the people I’m going to screw in the future.”

Under Macias’s leadership, a company called Home Recovery Trust was born. The Macias-Medina ring set up its business office in Rialto, one town west of the city of San Bernardino. The pair advertised their services in Hispanic communities, principally on TV and radio. Welch said that in Medina’s Spanish-language commercials, she “would tout herself as a successful woman.” At 23, she was young and attractive, a self-made immigrant. Welch noted that she would claim, “‘I used to be beaten by my husband, but I went out and took my own initiative and now I’m working for this great company, Home Recovery Trust, who can save your home.’ Then she outlined the program.”

Home Recovery Trust grew, Welch said, doing especially well in churches, where “Yunuen was very active” and where she’d offer seminars on alternatives to foreclosure. “A lot of our victims,” Welch said, “came from churches.” Soon, desperate homeowners were coming into the Rialto office and signing documents left and right.

The ring’s quitclaim deeds, falsely notarized by a woman named Reina Rogers, were transferred to the Michael Martinez Trust, another dummy entity. In addition, Home Recovery Trust required its clients to pay up-front fees (between $2500 and $3500) and make monthly rent or mortgage payments to the trust as well as sign powers of attorney.

Bank records showed that Macias and Medina took in more than $5 million. Maurice Landrum, senior investigator with the San Bernardino County district attorney’s office, said that Macias “personally withdrew” a little over $1 million “based on bank slips signed by him.”

Macias lived “like a rock star,” Welch said. “He rented a big portion of the Queen Mary to renew his vows with his wife,” bringing in guests via hired limo. He paid “$17,000 to rent a yacht. There were expensive hotels, clothes, the whole bit. If you had a chance then to see the victims — a blind lady, an elderly couple with a 35-year-old daughter in a wheelchair — and Macias was sitting across the table from them, saying, ‘We will save your house. Just keep sending us the money.’ It’s unconscionable. It’s just evil.”

In 2010, the Macias-Medina ring was busted. Ten people were arrested and all of them pled guilty.

Luis Macias was arrested April 20, 2010, in the hallway of the San Bernardino County superior courthouse, where he was facing, according to a district attorney’s press release, “felony charges in another real-estate-related fraud case.” For the felony charges with Home Recovery Trust he got five years and eight months in state prison. The trust was valued at $350,000, a paltry slice of the $5 million it had taken in. Restitution payments for the more than 450 victims have not yet been awarded.

Yunuen Medina served 180 days in county jail. She was then deported.

Big Day

The original ring involved David Zepeda and his brother John. About the time investigators were closing in on Macias and Medina, they were learning where the pair had gotten their training: from the mastermind David Zepeda.

The story of David Zepeda begins with his end — a day in August 2010 when Maurice Landrum had a crazy bit of luck. That day he happened to be checking crime reports. He found one that a David Zepeda had filed. Landrum knew the name. Sheriff’s deputies had been investigating Zepeda for real estate fraud, although they didn’t have his current address. Someone, Zepeda complained in the report, had thrown a rock through the window of his Bentley.

“Crooks always do something stupid to lead you to them.” Sheriff’s deputies found David Zepeda after he filed

a report that his Bentley had been vandalized.

Zepeda had bought a white Bentley sedan with white leather upholstery from Las Vegas Motor Cars and paid with a cashier’s check for $78,602. He’d parked the car in the driveway of his North Ofelia Drive home, located on a cul-de-sac in a new enclave in San Bernardino, close to the I-15 and I-215 merge. Eyeing window glass strewn through the Bentley’s lush interior, he called to report the crime so that his insurance would pay for the repair.

Though he was surprised, Landrum shouldn’t have been. “Crooks always do something stupid to lead you to them,” he said. He began surveillance and notified James Motz, an investigator for the real estate fraud division in the district attorney’s office in San Diego. Authorities here had gotten many complaints, as had the California Department of Real Estate, about loan-modification companies working in Vista, Fallbrook, Chula Vista, and elsewhere. The San Diego district attorney’s office had put Motz on the case.

On September 2, 2010, Landrum said that he, sheriff’s deputies, and Motz “hit the house.” Inside, they found John Zepeda. John, they didn’t know about. John said that David was in intensive care at Kaiser hospital in nearby Fontana. Leaving others to search the house, Landrum drove to the hospital and found David. Weighing nearly 300 pounds, in bed, and on a breathing tube, he had suffered a stroke one week earlier. San Diego court documents quote John Zepeda as saying at the time that doctors believed David “will neither walk nor talk again.”

Landrum arrived back at the house in time to hear John admitting to the real estate scheme with his brother. He began pulling out the drawers of his desk, then opened the safe in the master bedroom. He took investigators to a second bedroom where piles of forged documents lay. There they were — the fake notary stamps with the names of San Diego notaries Bill Washington, Karla and Joel Magana, Mark Desahagun, among many others. “It was unbelievable,” Landrum recalled. “If we hadn’t recorded it, nobody would have believed us.”

In the Zepeda brothers’ garage Landrum found a truck that contained a “treasure trove” of incriminating material. “The San Diego false [quitclaim] deeds, the San Bernardino false deeds, P.O. boxes in San Ysidro where the stuff was going — it was beautiful.”

In the meantime, investigator Motz got arrest warrants in San Diego for the brothers. They would be tried here first: the evidence of their crimes in San Diego County was strongest. Motz arrested John and David, although David had to remain in the hospital. Motz drove John to the San Diego jail.

Investigators found 8320 coins at Zepeda’s house, along with hundreds of thousands of dollars’ worth of cash, gold, jewelry, guns, and cashier’s checks.

From the house, the garage, and the truck, investigators collected $335,000 in cashier’s checks. In a closet they found a Thompson submachine gun, a Mossberg shotgun, and a Ruger Mini-14 with a folding stock. From the safe they catalogued a gold-colored Geneva watch, a gold-colored Rolex, and several diamond bracelets, necklaces, and rings. There was $31,502 in cash; 13 boxes of silver coins with 640 coins per box, totaling 8320; and several hundred boxes of gold troy ounces. In the end, the San Diego district attorney’s office collected 120 banker boxes of evidence, including records of quitclaim deeds from 400 homeowners; rent payments from many of those homeowners, made out to the David Zepeda Trust; and more than 400 forgeries of notary signatures on quitclaim deeds, all of which were filed with the San Diego County Recorder.

In a news conference at the time, district attorney Bonnie Dumanis charged the brothers with 106 felony counts as well as 215 “overt acts” of foreclosure fraud. The felonies included multiple counts each of conspiracy, forgery, using the personal identifying information of another, rent skimming, filing false instruments, and grand theft.

David Zepeda is now in custody in San Diego. Welch said that after the Zepeda brothers’ trials have finished in San Diego, he will file his case against them in San Bernardino. He is ready to go to trial with 74 counts against the brothers.

How the Zepedas Worked the Scheme

In early 2006, after David Zepeda formed Sunset Trust, changed later to Sunset Beach Management, he would drive around San Bernardino looking for distressed properties — anything to suggest a foreclosure in progress and an empty home. An overgrown yard, a cracked window, newspapers piling up in the driveway. Zepeda would place a For Rent sign, with his San Bernardino phone number, in the front yard.

He also researched foreclosure proceedings and contacted the underwater homeowner. He might, as a person commented on the Fallbrook Village News website, knock on the front door, “flash a badge [and say he was] employed . . . by a city’s code enforcement division.” Then he would tell the distressed owner that he knew of a company, Sunset Beach Management, that could save his or her property.

In his criminal complaint, Motz described the scheme. Once the Zepeda brothers identified a foreclosure, they had the homeowner sign a quitclaim deed or John would forge one, and John would forge the name of a local notary onto the deed: the names could not be fabricated because the county recorder’s office would check both names when the deed was filed.

Next, Motz wrote, David Zepeda “rents out the property, in most cases for over a thousand dollars per month.” To “forestall the foreclosure process,” he would transfer the property from one trust to another. He would also buy time — to collect more rent — by filing a bankruptcy petition for the homeowner. “Money is diverted away from the lenders and owners and into Zepeda’s accounts,” Motz wrote. “Zepeda then uses the rent money to support a lavish lifestyle, including the purchase of multiple luxury, high-end automobiles and travel.”

The Torres Family Joins the Circus

Maurice Landrum described yet another ring — a third — composed of Carlos Torres, his sister Patricia, and their father Manuel. Carlos had “learned the Zepedas’ system and branched out” on his own in San Diego. Oscar Macias (unrelated to Luis Macias) was an associate of the Torreses and the Zepedas.

In San Diego, the Torres ring filed about a dozen quitclaim deeds, transferring property to the Carlos Torres Trust. In San Bernardino, two of the people Carlos defrauded were law enforcement officers, who, according to the district attorney’s press release, “were unaware that their names had been forged on quitclaim deeds, or their properties had been rented out.”

After multiple investigations in 2009 and 2010, the case went to the San Bernardino grand jury. Arrest warrants were issued for, among others, Carlos, Patricia, and Manuel Torres and their associate Oscar Macias.

In spring 2010, Landrum arrested Carlos Torres at the federal prison at Lompoc. Torres was serving a two-year sentence, having pled guilty to another charge — conspiracy to transport illegal aliens in California. Vance Welch, San Bernardino deputy district attorney, said that “Carlos is into a lot weirder stuff than we just had him for.”

In San Bernardino superior court, Carlos Torres pled guilty on June 10, 2010, to forgery and conspiracy to commit felony real estate fraud. He received two years in a state prison. The father, Manuel, pled guilty to the same charges, got 120 days in county jail, and received three years’ felony probation. Oscar Macias, a stout, shaved-head bagman, also pled guilty and received time served.

In October of 2010, prosecutors in San Diego indicted David Zepeda, Carlos Torres, and Patricia Torres on charges of forgery, conspiracy, and filing false documents.

It’s not a stretch to say that San Bernardino deputy district attorney Welch sounds livid, thinking back on five years of the Southland’s big uptick in foreclosure fraud. “Sometimes I feel like I’m standing on a beach holding back a wave,” he says. San Diego has been the “only county” to cooperate in investigating and prosecuting these multijurisdictional crimes. Neither his office nor San Diego’s, he says, has the resources to nail every fraudulent loan modifier. “We will pick and choose where [prosecutions] will make the greatest impact and that will send the message that you don’t do it here.”

Welch says he wishes that more county and state officials would get involved. But, he notes, the “egos are just too big” in Los Angeles, Riverside, and Orange counties for their fraud divisions to collaborate with him. What’s more, recent and current attorneys general — Jerry Brown and Kamala Harris — promised to prosecute these illegal rings but so far they have not. “Everything we referred to the [state] attorney general’s office got sent back.”

The State’s Oversight

The California Department of Real Estate issues a “desist and refrain” order when an investigation reveals that people who do not have a real estate license are acting as real estate brokers. This includes negotiating the sale of real property, soliciting for prospective tenants, and performing services for borrowers in connection with loans secured by liens on real property. Operating without a license is a violation of the California Business and Professions Code. David Zepeda and 34 other people, trusts, and businesses were ordered on January 26, 2012, to desist and refrain from performing acts for which a real estate broker license is required.

The department of real estate investigation found that at least 550 Southern California homeowners have been victimized by the Zepeda brothers. One variation of the loan-modification scheme was called the “caretaker plan.” The homeowner quitclaims their house, bequeathing it to a trust, and pays rent and fees to the trust. They’re told that once the trust collects several deeds, its trustees will pool the “homeowner monies” in order to purchase the notes from the homeowners’ lenders. Eventually, the trust, so the plan goes, sells the property back to the homeowner at a lower cost. The problem is, such packaging, which sounds good to a distressed debtor, is all shine. There is no pool of money to purchase the homes. The money has been spent. Plus there is no modified loan that can be negotiated between lender and homeowner. No bank is involved. The caretaker plan is styled as a way to buy time and to keep the property from foreclosure. Just the opposite occurs. Most homeowners lose their properties to foreclosure and are evicted.

Tom Pool, spokesperson for the department of real estate, says there are several reasons why foreclosure fraud has mushroomed in the past five years. First, lenders have not had the resources to deal with the volume of defaults, late payments, and requests for loan modifications. Second, federal and state laws, some enacted as the crisis developed, require lenders to make mortgage adjustments, though much anecdotal evidence suggests that adjustments are not being made. (SB 1137, a mortgage relief bill passed in 2008, requires that lenders contact delinquent homeowners and negotiate a loan modification 30 days before sending them a notice of default.) Then there are delays the law requires: notice of default, a 90-day waiting period before the foreclosure process begins, and more. Add to that a bankruptcy filing on the part of a homeowner or trust, again to buy time, and one founders in the swamp of delay. With such a bog of rules, the average time it takes a foreclosure to be processed is 260 days.

One Little Fish, One Big Piranha

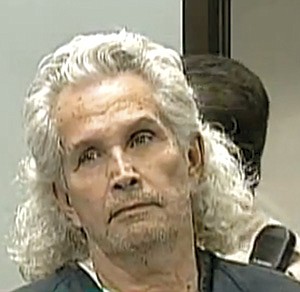

One of the many curiosities about John Zepeda, who reached a plea agreement with San Diego prosecutors in December of 2011, is that his attorney, deputy public defender Kathleen Coyne, insisted that he was only peripherally involved. John was David’s notary forger — just an employee. In his San Bernardino home office, he made the fake notary stamps, then stamped them on the fake quitclaim deeds and forged the notary’s signature. He was a little fish compared to David, the piranha, so Coyne said. But the judge didn’t buy her defense. After John pled guilty to 13 felony counts — using personal information of another, forging checks and money orders, filing false instruments, and rent skimming — the judge sentenced him to 12 years in state prison, minus the 534 days that he'd already been locked up.

John Zepeda in court

The “restitution floor amount” in the Zepeda brothers’ case has been put at $6 million in San Diego. The district attorney’s office has put the number of local victims at 40, with 26 properties involved. And yet the worth of the Zepeda brothers’ ring, which overlaps with the Torres family ring, is estimated at only $200,000 or $300,000, similar to the Macias-Medina ring. As part of John Zepeda’s sentence, the judge ruled that the fine against him be reduced from $10,000 to $200. This ruling makes more money — but not much — available for victims. Whether or not those victims, which includes the lending institutions, will get any money remains to be seen. The court assigns a forensic accountant to cull through those 120 boxes and unravel the web of bank accounts. The restitution hearings won’t occur until after David Zepeda’s trial.

San Diego Crooks Finally Sentenced

For months of hearings, Patricia Torres came to court wearing an ankle lock, its green light flashing. In April, she pled guilty, her agreement including a maximum of six years in state prison. She will be sentenced July 13.

The same month, her brother Carlos pled guilty to conspiracy and was sentenced to three years and four months. This term is to be served consecutively with the time remaining on his federal sentence for transporting illegal aliens into the country.

In part because of David Zepeda’s stroke, his fragile health, and the complexity of the case, his defense attorneys have asked the court several times to postpone their client’s trial. At hearings in which Zepeda has appeared, the wait to begin is extra long. He must be transported from a local facility where ill prisoners are kept. The bailiff brings him in in a wheelchair. Zepeda is slumped and motionless. His gray beard and graying sidewalls, his eerie stillness, give him a near-hospice look. The bailiff announces to the judge that Zepeda can’t hear well: attorneys must stand near him and state charges and motions in a mild shout. His trial is currently scheduled to begin on July 23.

Comments