{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Big Four accounting firms do dirty work

U.S. Financial, Westgate used 'em

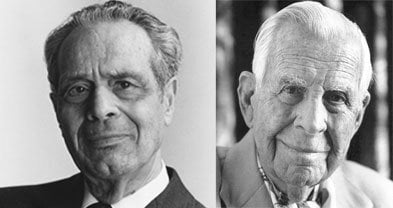

Gadfly Abraham Briloff (left) helped expose infamous San Diego accounting scandals such as C. Arnholt Smith’s (right) U.S. National Bank debacle.

The accounting profession has stark similarities with the world’s oldest profession. Both attempt to operate below the radar, asking few probing questions of their clients. This has been going on a long time, as the histories of El Cajon Boulevard and local financial shenanigans reveal.

Last month, the Public Company Accounting Oversight Board, in an unprecedented move, slammed the Big Four accounting firm of Deloitte & Touche for relying too much on its clients’ word when doing audits; in short, see no evil, hear no evil, speak no evil when blessing a dubious client’s accounting.

Congress created the oversight board in 2002 after accounting scams such as Enron rocked the nation.

Decades ago, the major accounting firms were known as the Big Eight. Then, as mergers multiplied, there was the Big Six and then the Big Five. After Arthur Andersen, accountant for Enron and San Diego’s scandal-plagued Peregrine Systems, lost its license, the Big Four was left standing — wobbly.

Predecessor firms of Deloitte & Touche were involved in two of San Diego’s biggest accounting scandals, both hitting the headlines in 1973: U.S. Financial and C. Arnholt Smith’s U.S. National Bank and Westgate-California.

Touche Ross was the auditor for U.S. Financial, a high-flying real estate company of the 1960s and early 1970s. Profits seemingly soared as the stock zoomed above $60. But Abraham Briloff, a New York accounting professor and the industry gadfly, declared that the company was a Potemkin village. In his books and in articles in Barron’s, he exposed accounting frauds. Just a rumor that Briloff was planning a Barron’s article could send a stock plummeting. He pricked U.S. Financial’s balloon in a Barron’s article.

Briloff’s favorite story (apocryphal) was about a company choosing an accounting firm. The chief executive interviewed representatives of all the Big Eight, asking each a question: “What does two plus two equal?” Partners of seven firms unhesitatingly replied, “Four, of course.”

But the partner of the eighth firm, after a long pause, replied, “What number did you have in mind?” His firm got the account.

As Briloff and federal regulatory and criminal agencies pointed out, U.S. Financial would sell products to its own subsidiaries, thus pushing up reported profits. That’s a no-no. Then, U.S. Financial would sell out a development before it opened. It would book the expected future revenue, then estimate the expenses — usually understating them, thereby boosting profits artificially.

The company went bankrupt in mid-1973; ultimately, three executives went to prison for financial fraud, and several other executives got lesser penalties. The auditor, Touche Ross, had to pay a bundle of money to settle civil fraud suits. The Securities and Exchange Commission censured the accounting firm and barred its San Diego office from accepting publicly held companies as audit customers for one year. The government agency told Touche to adopt procedures to determine “management’s direct or indirect involvement in material transactions which are included in the financial statements.” That is, “Look out for insider hanky-panky.”

A second legendary San Diego accounting fraud involved the same thing: management’s direct or indirect involvement in material transactions. Half a century ago, C. Arnholt Smith was “Mr. San Diego,” controlling U.S. National Bank and Westgate-California, a conglomerate including a tuna company, hotels, Yellow Cab operations, an airline, and real estate. But the Securities and Exchange Commission said that Smith and his cronies had concocted a scheme to engage in sham transactions to pump up profits of both the bank and Westgate.

Smith and his close colleagues, along with relatives, owned and controlled a slew of assets that would be traded back and forth at inflated prices. The bank would do the financing. The Securities and Exchange Commission pointed out that these deals were put together to hoodwink auditors into believing the transactions were at arm’s length — when in fact they were dubious deals among friends and relatives.

This mare’s nest of deals caused another problem: the bank’s loans to Smith associates vastly exceeded bank regulators’ limits on insider transactions. The United States Comptroller of the Currency said the bank’s muddle of Smith-related transactions was “self-dealing run riot.”

In a 1973 speech in San Diego, Briloff laughed that there must be a gnome that burrowed under the downtown street between the bank and the conglomerate, delivering the assets to whichever place the auditors happened to be.

Westgate went into bankruptcy, and its various entities were sold off. The bank was seized by the federal government in mid-1973. Smith went into custody, albeit briefly.

And what about those accounting firms that the rickety structure was set up to deceive? Westgate went through four accounting firms in four years. One was Haskins & Sells, which eventually became part of Deloitte. Haskins attached a bunch of footnotes to the 1970 Westgate annual report. The accounting firm noted that it had not been able to verify a lot of Westgate’s claimed activities. That 1970 report disclosed numerous transactions that had not been made public before. Smith fired the firm and told shareholders that he was unhappy with those footnotes.

Then, for the 1971 report, he hired Touche Ross. It couldn’t cut through the haze, either, and said so in the annual report. Smith fired Touche.

All told, the Deloitte & Touche predecessors performed dismally in U.S. Financial but did reasonably well in dissecting Smith’s jerry-built empire.

The successor firm, Deloitte & Touche, has been auditor in some of America’s biggest financial scams, including Washington Mutual, Bear Stearns, and Adelphia Communications. It has dodged liability in some lawsuits but has had to shovel out bucks in others. The other three of the Big Four — PricewaterhouseCoopers, Ernst & Young, and KPMG — have been involved in questionable accounting for shady clients but haven’t been ticketed by the Public Company Accounting Oversight Board.

Here's something you might be interested in.

Big Four accounting firms do dirty work

U.S. Financial, Westgate used 'em

Big Four accounting firms do dirty work

U.S. Financial, Westgate used 'em

Gadfly Abraham Briloff (left) helped expose infamous San Diego accounting scandals such as C. Arnholt Smith’s (right) U.S. National Bank debacle.

The accounting profession has stark similarities with the world’s oldest profession. Both attempt to operate below the radar, asking few probing questions of their clients. This has been going on a long time, as the histories of El Cajon Boulevard and local financial shenanigans reveal.

Last month, the Public Company Accounting Oversight Board, in an unprecedented move, slammed the Big Four accounting firm of Deloitte & Touche for relying too much on its clients’ word when doing audits; in short, see no evil, hear no evil, speak no evil when blessing a dubious client’s accounting.

Congress created the oversight board in 2002 after accounting scams such as Enron rocked the nation.

Decades ago, the major accounting firms were known as the Big Eight. Then, as mergers multiplied, there was the Big Six and then the Big Five. After Arthur Andersen, accountant for Enron and San Diego’s scandal-plagued Peregrine Systems, lost its license, the Big Four was left standing — wobbly.

Predecessor firms of Deloitte & Touche were involved in two of San Diego’s biggest accounting scandals, both hitting the headlines in 1973: U.S. Financial and C. Arnholt Smith’s U.S. National Bank and Westgate-California.

Touche Ross was the auditor for U.S. Financial, a high-flying real estate company of the 1960s and early 1970s. Profits seemingly soared as the stock zoomed above $60. But Abraham Briloff, a New York accounting professor and the industry gadfly, declared that the company was a Potemkin village. In his books and in articles in Barron’s, he exposed accounting frauds. Just a rumor that Briloff was planning a Barron’s article could send a stock plummeting. He pricked U.S. Financial’s balloon in a Barron’s article.

Briloff’s favorite story (apocryphal) was about a company choosing an accounting firm. The chief executive interviewed representatives of all the Big Eight, asking each a question: “What does two plus two equal?” Partners of seven firms unhesitatingly replied, “Four, of course.”

But the partner of the eighth firm, after a long pause, replied, “What number did you have in mind?” His firm got the account.

As Briloff and federal regulatory and criminal agencies pointed out, U.S. Financial would sell products to its own subsidiaries, thus pushing up reported profits. That’s a no-no. Then, U.S. Financial would sell out a development before it opened. It would book the expected future revenue, then estimate the expenses — usually understating them, thereby boosting profits artificially.

The company went bankrupt in mid-1973; ultimately, three executives went to prison for financial fraud, and several other executives got lesser penalties. The auditor, Touche Ross, had to pay a bundle of money to settle civil fraud suits. The Securities and Exchange Commission censured the accounting firm and barred its San Diego office from accepting publicly held companies as audit customers for one year. The government agency told Touche to adopt procedures to determine “management’s direct or indirect involvement in material transactions which are included in the financial statements.” That is, “Look out for insider hanky-panky.”

A second legendary San Diego accounting fraud involved the same thing: management’s direct or indirect involvement in material transactions. Half a century ago, C. Arnholt Smith was “Mr. San Diego,” controlling U.S. National Bank and Westgate-California, a conglomerate including a tuna company, hotels, Yellow Cab operations, an airline, and real estate. But the Securities and Exchange Commission said that Smith and his cronies had concocted a scheme to engage in sham transactions to pump up profits of both the bank and Westgate.

Smith and his close colleagues, along with relatives, owned and controlled a slew of assets that would be traded back and forth at inflated prices. The bank would do the financing. The Securities and Exchange Commission pointed out that these deals were put together to hoodwink auditors into believing the transactions were at arm’s length — when in fact they were dubious deals among friends and relatives.

This mare’s nest of deals caused another problem: the bank’s loans to Smith associates vastly exceeded bank regulators’ limits on insider transactions. The United States Comptroller of the Currency said the bank’s muddle of Smith-related transactions was “self-dealing run riot.”

In a 1973 speech in San Diego, Briloff laughed that there must be a gnome that burrowed under the downtown street between the bank and the conglomerate, delivering the assets to whichever place the auditors happened to be.

Westgate went into bankruptcy, and its various entities were sold off. The bank was seized by the federal government in mid-1973. Smith went into custody, albeit briefly.

And what about those accounting firms that the rickety structure was set up to deceive? Westgate went through four accounting firms in four years. One was Haskins & Sells, which eventually became part of Deloitte. Haskins attached a bunch of footnotes to the 1970 Westgate annual report. The accounting firm noted that it had not been able to verify a lot of Westgate’s claimed activities. That 1970 report disclosed numerous transactions that had not been made public before. Smith fired the firm and told shareholders that he was unhappy with those footnotes.

Then, for the 1971 report, he hired Touche Ross. It couldn’t cut through the haze, either, and said so in the annual report. Smith fired Touche.

All told, the Deloitte & Touche predecessors performed dismally in U.S. Financial but did reasonably well in dissecting Smith’s jerry-built empire.

The successor firm, Deloitte & Touche, has been auditor in some of America’s biggest financial scams, including Washington Mutual, Bear Stearns, and Adelphia Communications. It has dodged liability in some lawsuits but has had to shovel out bucks in others. The other three of the Big Four — PricewaterhouseCoopers, Ernst & Young, and KPMG — have been involved in questionable accounting for shady clients but haven’t been ticketed by the Public Company Accounting Oversight Board.

Comments