{kind=link}

Sponsored

Sponsored

On May 11, the oft-bashed bureaucrats who supposedly regulate the securities industry finally could smile: the Justice Department convicted billionaire hedge fund operator Raj Rajaratnam of criminal insider trading. The Securities and Exchange Commission, which has come under the most criticism but doesn’t have criminal powers, had charged Rajaratnam and a ring of insiders with the same offense two years earlier.

But two days after the Rajaratnam conviction, Friday the 13th, the Securities and Exchange Commission was double-demonized — deservedly. First, a House financial subcommittee held a hearing on why the commission had dropped the ball in pursuing R. Allen Stanford, a Houston financier charged with running a $7 billion Ponzi scheme. And then a watchdog group published a scathing study of the incestuous relationship between the commission and Wall Street.

The subcommittee heard how a female employee of the agency’s Fort Worth office had repeatedly tried to get her bosses to look into the preposterous returns Stanford was promising investors. She got a letter of reprimand and was transferred to another position. The securities agency lawyer who kept blocking investigations of Stanford quit the government and went to work for — you guessed it — Stanford.

It was a classic example of the revolving door by which Wall Street investment and law firms control the securities commission, the primary regulator of stock and bond activity. Agency lawyers in charge of a big investigation get hired by the law firm representing the crook. The result is that the market finaglers go free and the ex–government lawyers rake in $2 million or more a year defending the kinds of bandits they formerly chased.

That was the subject of the second Friday the 13th smackdown of the commission. The Project on Government Oversight, a watchdog organization, released a major study on the revolving-door phenomenon.

An agency lawyer who goes to the private sector must file a statement if he or she intends to represent a client before the commission within two years of departing. Under the Freedom of Information Act, researchers at the Project learned that between 2006 and 2010, a full 219 former securities commission employees had filed such statements.

The revolving door has often been a factor in thwarting securities-fraud investigations and can work in subtle ways, concluded Project researchers. A law firm may dangle a juicy job in front of an agency lawyer who is merely thinking of investigating the firm’s client. The law firm may have its ex–government attorneys try to sway former colleagues in an investigation.

In one section of its report, the Project on Government Oversight asks, “Does the Revolving Door Undermine [Securities and Exchange Commission] Enforcement and Regulatory Actions?” Then the watchdog answers its own query by citing several cases — one of which, involving San Diego attorney Gary Aguirre, has become a black mark on the agency’s history.

Growing restless after retiring from a lucrative law practice, Aguirre joined the Securities and Exchange Commission several years ago.

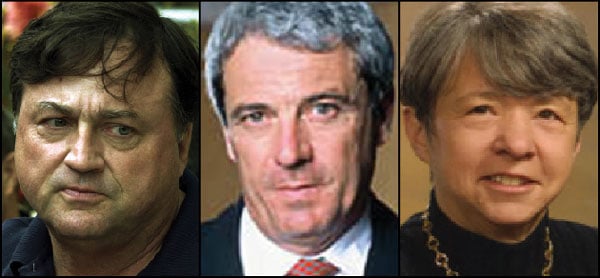

He began looking into a possible insider trading case. Pequot Capital Management, once the world’s biggest hedge fund, had made a bundle betting on the stock of a financial company just before it announced it would be acquired at a fat premium. Pequot had also bet that the stock of the acquirer would go down; that normally happens when a company makes an acquisition. Wall Street powerhouse John Mack, Pequot’s former chairman and a large investor in the hedge fund, had recently talked with the investment banking firm handling the acquisition. Mack was a close friend of Pequot’s chief executive, Arthur Samberg. Aguirre thought Mack should be interviewed. Did he pass nonpublic information on the pending acquisition to Samberg? After all, Pequot had made many other suspicious trades. Aguirre’s boss at the commission noted that Mack had “very powerful political connections,” according to the Project report. Indeed, Mack had raised $200,000 for George W. Bush in 2004.

Suddenly, Aguirre was fired. At the time, Wall Street giant Morgan Stanley was thinking of hiring Mack as its chief executive. The big law firm Debevoise & Plimpton was hired to vet Mack. Debevoise began asking top officials at the securities agency whether Mack might be besmirched in an investigation. Mary Jo White, who as U.S. attorney for the Southern District of New York had been responsible for policing Wall Street but was now making huge bucks working for Debevoise, covertly contacted senior agency personnel, including the enforcement chief, on Mack’s behalf, according to Project investigators, quoting an earlier Senate committee investigation of the matter.

Paul Berger was an agency official a couple of notches above Aguirre. He signed the papers authorizing Aguirre’s firing. Berger had a supervisory role in the Pequot/Mack investigation, such as it was, and White conferred with him. “Berger contacted Debevoise & Plimpton about potential employment just days after he initialed Aguirre’s termination notice,” according to the Senate investigation. “Berger did not recuse himself until four months later,” just before he took a fat job with Debevoise. “It appears that the [Securities and Exchange Commission] did very little to investigate Mack’s potential role in the period between Aguirre’s firing in September 2005 and Berger leaving the commission in the spring of 2006,” said the Senate report, which concluded that Berger did not recuse himself in a timely manner and was “less than forthcoming” in the investigation.

According to the Senate probe, Berger worked through an intermediary, one Lawrence West, another agency lawyer. Senate investigators unearthed an email from West to Berger in late 2005. The subject line read: “Debevoise.” The note read, “Mary Jo [White] just called. I mentioned your interest.” Berger admitted that West had been the go-between in the Debevoise contact.

Who is Lawrence West? Well, he was the primary securities agency lawyer on the Peregrine Systems scam. John Moores, former major owner of the Padres and also onetime chairman of Peregrine, hired Charles La Bella, former United States attorney, to quarterback a report on the Peregrine swindle. Not surprisingly, the report, by the law firm Latham & Watkins, exonerated boardmembers, including Moores. At the securities commission, West gave his blessings to the Latham & Watkins report, widely considered a whitewash. Then, within four months of assisting Berger to get a job at Debevoise, West joined Latham & Watkins.

I gave both lawyers a chance to refute anything in the Project and Senate reports and asked West to explain how he landed at Latham & Watkins, but heard nothing.

The sordid story does have a happy ending — of sorts. Investigations by two Senate committees and the agency’s own internal watchdog vindicated Aguirre and slammed the securities commission for not pursuing Mack diligently. Working on his own, Aguirre gave more insider trading evidence on Pequot to the red-faced securities agency. Reluctantly, it banned Samberg from the business, fined him and Pequot $28 million (a pittance since Samberg was worth $15 billion), and paid Aguirre $755,000 in a lawsuit settlement. Pequot closed down. But Mack, White, Berger, and West are doing swimmingly. And so, unfortunately, is the Securities and Exchange Commission — even after Friday the 13th.